The Reserve Bank of India (RBI) has rolled out its Credit Information Reporting Directions, 2025, a significant step toward making credit reporting more reliable, accurate, and transparent. Here’s a breakdown of what it means for borrowers and lenders.

What’s the New Rule About?

This updated framework consolidates and improves previous guidelines for sharing and updating credit information. It aims to ensure that lenders (Credit Institutions or CIs) and credit bureaus (Credit Information Companies or CICs) provide timely, accurate, and standardized data about borrowers.

The Credit Information Companies Regulation Act, 2005 (CICRA) empowers CICs like CIBIL, Experian, CRIF High Mark and Equifax to collect and disseminate credit data from CIs. With the growth of credit penetration and digital lending in India, timely updates of credit data have become critical. However, challenges like delayed data submissions, discrepancies in credit histories, and inadequate grievance redressal mechanisms have persisted.

To address these gaps, the RBI introduced this Master Direction, which replaces several earlier guidelines and strengthens compliance requirements for both CIs and CICs.

Key Highlights of the Framework

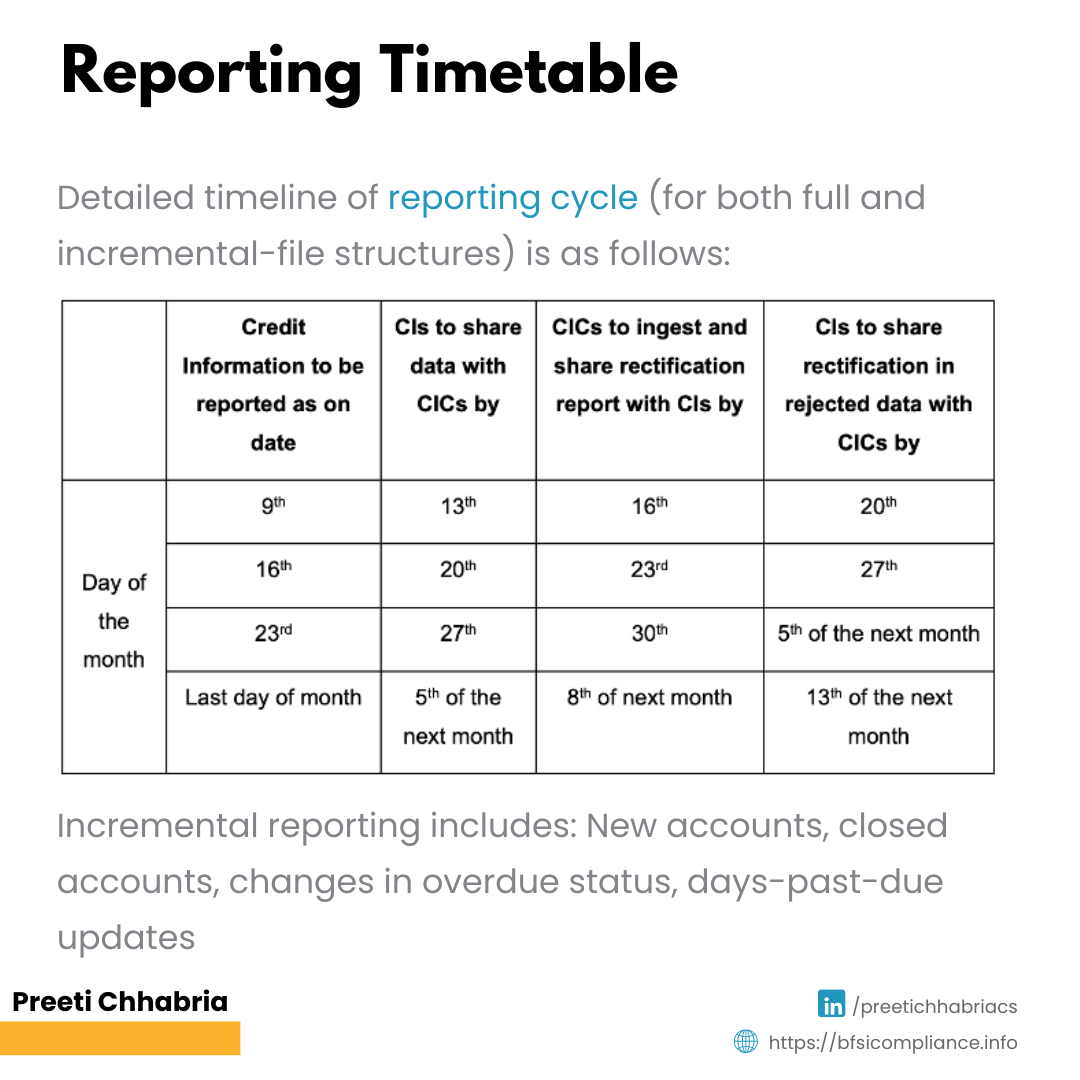

• Credit institutions must update borrowers’ credit information on a fortnightly basis, i.e., on the 15th and the last day of each month.

• These updates must be transmitted to credit bureaus within 7 calendar days of the relevant reporting fortnight to ensure timely data availability.

• Borrowers’ financial details, including PAN, corporate information (based on CIN), and directors’ credit histories (based on DIN), must be comprehensively reported.

• Accounts will be categorised as settled or disputed accounts to avoid misunderstandings in credit reports.

• Older account data (pre-2018) will be transitioned into modern formats to improve consistency.

• The process of credit data sharing now has legal backing, eliminating the need for borrowers’ consent.

• Complaints from borrowers, particularly those concerning credit data errors, must be resolved within 30 days. Institutions failing to do so must compensate the borrower at a rate of ₹100 per day.

• Lenders should refrain from rejecting first-time borrowers solely due to the absence of credit history.

• It is essential to include comprehensive customer data through unique identifiers such as PAN or Voter ID to ensure accuracy and completeness.

What Does This Mean for Borrowers?

• The shift to a fortnightly update cycle ensures that borrowers’ credit scores reflect their most recent financial activities. This timely reporting provides borrowers with a clearer and more accurate understanding of their financial health.

• Additionally, the framework enhances transparency by enabling borrowers to monitor their credit reports more effectively and make informed financial decisions.

• The emphasis on grievance redressal ensures that errors in credit data are resolved promptly. Further, the provision of financial compensation for delays safeguards the interests of borrowers and strengthens accountability among credit institutions.

Why Is This Important for Lenders?

• For lenders, the updated guidelines provide access to more current and comprehensive credit information. This enhances their ability to assess and mitigate credit risk effectively, thereby reducing the likelihood of defaults.

• The improved reporting standards and streamlined processes ensure that lenders have reliable data to support their lending decisions, particularly in the case of first-time borrowers.

• Furthermore, by adhering to these best practices, lenders can foster a more transparent, trustworthy, and efficient credit ecosystem, ultimately contributing to greater financial stability.

The Bigger Picture

These new rules are designed to build trust in India’s credit system. Borrowers benefit from more transparency and faster resolutions, while lenders gain tools to make smarter, data-backed decisions.

As India’s credit landscape evolves, the RBI’s move ensures that everyone—from individuals to businesses—has a fair and efficient credit ecosystem to rely on.

Follow me on LinkedIn for more information and subscribe for updates on compliance, NBFCs, BFSI, etc.

Subscribe to my newsletter directly to your email inbox: https://bfsicompliance.info/subscribe-for-alerts/