India’s financial sector is navigating major regulatory changes impacting NBFCs, microfinance institutions (MFIs), and banks. While the RBI has eased some lending restrictions to improve liquidity, concerns over credit risks and financial stability persist.

Why Risk Weight Cuts Now and the Background

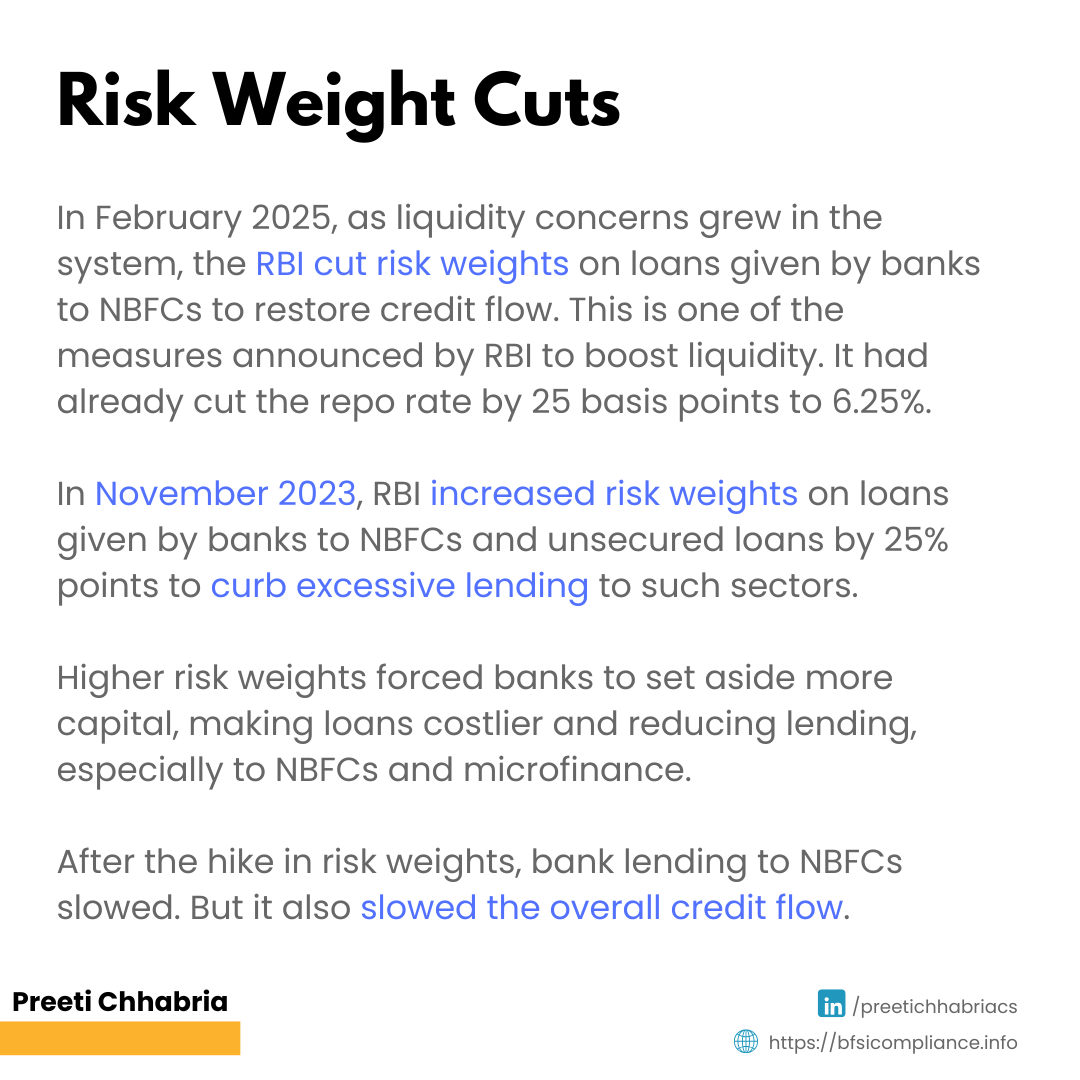

1. Background - RBI Increased Risk Weights in Nov 2023

In November 2023, the RBI raised risk weights on bank loans to NBFCs (from 100% to 125%) and consumer credit (from 100% to 125%) to curb excessive unsecured lending. Personal loans and credit card debt were growing over 20% annually, and defaults were rising. To control defaults and excessive risky lending, the RBI increased risk weights. Higher risk weights forced banks to set aside more capital, making loans costlier and reducing lending, especially to NBFCs and microfinance institutions.

2. Impact of the Hike in Risk Weights Done in Nov 2023

Bank lending to NBFCs slowed, falling from 15% YoY in 2023 to 6.7% in 2024. Lending to NBFCs other than housing finance companies (HFCs) fell from 18.8% YoY in 2023 to 9.3% YoY in 2024.

Source: Economic Times

3. Latest Step by RBI in 2025 – Rollback in Risk Weights

By February 2025, as liquidity concerns grew, the RBI cut risk weights to restore credit flow:

• AAA-rated NBFC loans: Risk weight reduced from 45% to 20%

• Microfinance loans: Lowered from 125% to 100%

The reduction in risk weights is expected to free up about ₹40,000 crore in capital, allowing banks to lend up to ₹4 lakh crore to AAA-rated companies, as reported in Economic Times.

This was the regulator’s second action in less than a month to support growth, after lowering the repo rate by 25 basis points to 6.25% on February 7. A reduction in repo rate increases liquidity in the system and leads to lower lending rates.

However, the question remains:

What about Non-AAA Rated NBFCs?

Will they continue to experience slower growth due to liquidity challenges?

Does Relaxation in Risk Weight Signal Risk Is Over?

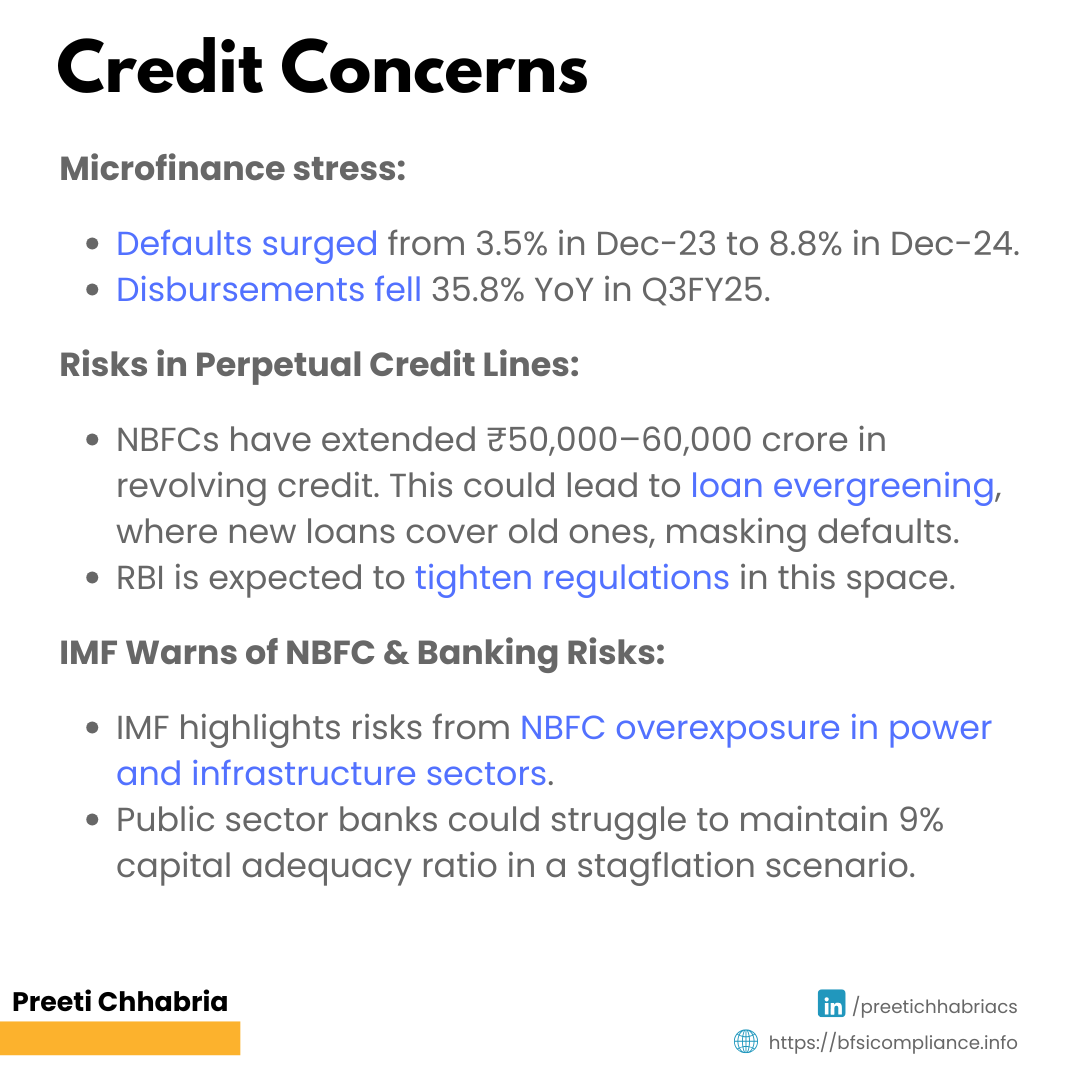

Despite lower risk weights, banks remain hesitant to expand microfinance lending due to rising defaults. The Portfolio at Risk (PAR) for loans overdue by 30+ days surged to 8.8% in December 2024 from 3.5% a year earlier. Liquidity issues and weaker incomes further dampen credit demand.

Adding to the slowdown, from April 1, 2025, a new MFIN rule will limit borrowers to three lenders instead of four, further restricting credit growth. Loan disbursements are already down 35.8% YoY in Q3 FY25.

Experts predict banks will wait for better repayment trends before scaling up microfinance lending.

What More – Sebi Expands NBFC Investment Scope

To boost liquidity in the distressed asset market, Sebi now allows all NBFCs, including HFCs, to invest in Security Receipts (SRs) issued by Asset Reconstruction Companies (ARCs). This move widens the investor base and prevents defaulting promoters from reclaiming assets through SR investments.

RBI Flags Concerns Over Perpetual Credit Lines

The RBI has raised concerns over NBFCs offering perpetual credit lines, where borrowers can withdraw and repay indefinitely, similar to cash credit facilities. Such products could lead to loan evergreening, a practice where new loans repay old ones, hiding defaults.

NBFCs have already extended ₹50,000–60,000 crore via such credit lines to salaried individuals, small business owners, and self-employed borrowers. The RBI is expected to tighten regulations in this space.

IMF Warns of NBFC Stress and Systemic Risks

The IMF’s India Financial System Stability Assessment report highlights risks from NBFC overexposure to power and infrastructure lending:

• The top three Infrastructure Financing NBFCs now hold 63% of power sector loans, up from 55% in FY20

• They rely on market borrowings for 56% of their funding, exposing them to liquidity shocks

• State-owned NBFCs like IREDA face higher risks and need stronger regulatory oversight

The IMF also flagged risks for public sector banks (PSBs) in a stagflation scenario, noting that many could struggle to maintain the 9% Capital Adequacy Ratio (CAR). It suggested that PSBs retain earnings instead of paying dividends to strengthen their capital base.

Will the government be comfortable with it?

Balancing Growth and Stability

While the RBI’s easing of risk weights should improve liquidity, challenges remain. Rising microfinance defaults, NBFC overexposure, and unregulated credit lines could pose financial risks.

The IMF’s warnings highlight the need for cautious lending and stronger capital buffers. The coming months will test whether these regulatory shifts successfully balance credit growth with financial stability.

Follow me on https://www.linkedin.com/in/preetichhabriacs/

for more information and subscribe for updates on compliance, NBFCs, BFSI, etc.

Subscribe to my newsletter directly in your inbox: