In one of the previous newsletters, we discussed Know Your Customer (KYC) norms in India and how any organisation implements them through the Governance, Risk Management and Compliance (GRC) framework. In today’s newsletter, we will take a comprehensive look at key differences in global KYC regulations in Section 1, and specifically, in the new-age frontier and challenger cryptocurrencies or virtual digital assets in Section 2.

Section 1: Key Differences in KYC Rules in the US, EU, India, and China

The approach to KYC compliance varies significantly across major jurisdictions. While all regions aim to combat money laundering and terrorist financing, their legal frameworks, enforcement mechanisms, privacy standards, and risk assessment models differ.

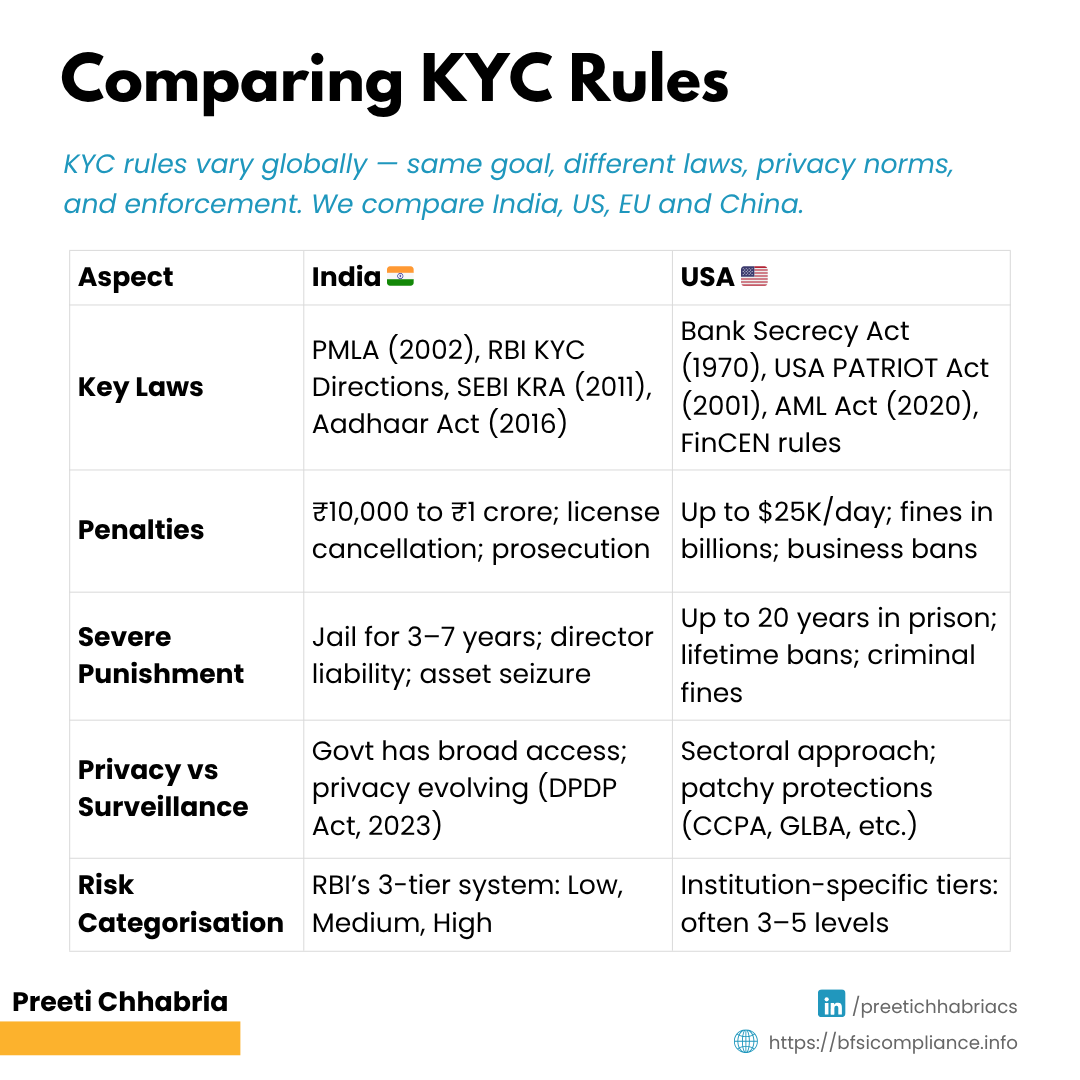

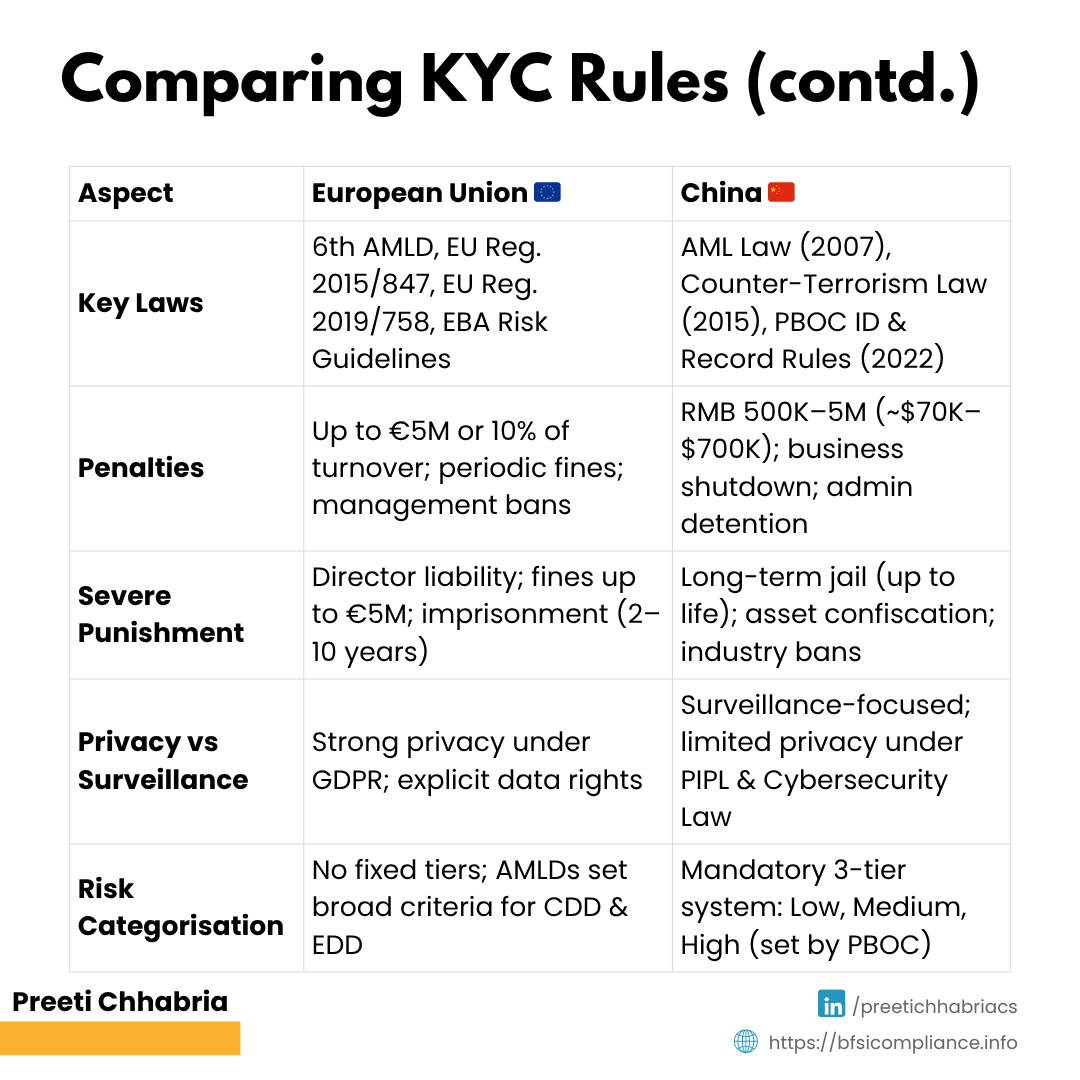

The table below compares India, the US, the EU, and China across key aspects such as governing laws, penalties, severity of punishment, privacy considerations, and risk categorisation methods.

| Aspect | India | USA | European Union | China |

|---|---|---|---|---|

| Laws | Prevention of Money Laundering Act (2002); RBI KYC Master Direction; SEBI KYC Registration Agency Regulations (2011); Aadhaar Act (2016) | Bank Secrecy Act (1970); USA PATRIOT Act (2001); CDD Final Rule (2016/2018); Anti-Money Laundering Act (2020); FinCEN regulations | 6th Anti-Money Laundering Directive; EU Regulation 2015/847; EU Regulation 2019/758; EBA Guidelines on Risk Factors | Anti-Money Laundering Law (2007); Customer ID and Record-keeping Measures (2007); Client ID and Transaction Recording Measures (2022); Counter-terrorism Law (2015); PBOC AML/CFT regulations |

| Penalties for non-compliance | ₹10,000 to ₹1 crore ($1,200-$120,000); Deposit acceptance prohibition; License cancellation, etc. | Up to $25,000/day per violation; Fines reaching billions for serious cases; Activity restrictions, etc. | Up to €5 million or 10% of annual turnover; Periodic penalty payments; Temporary management bans, etc. | RMB 500,000 to 5 million ($70k-$700k); Business suspension; Administrative detention, etc. |

| Severe punishments | Criminal proceedings against directors; 3-7 years imprisonment; Director personal liability; etc. | Criminal prosecution; Up to 20 years imprisonment; Lifetime industry bans; etc. | Personal fines up to €5 million; Director liability; Imprisonment (2-10 years); etc. | Long-term imprisonment (up to life); Lifetime industry bans; Asset seizure/confiscation; etc. |

| Privacy vs. Surveillance balance | Evolving privacy framework with significant government access [Digital Personal Data Protection Act (2023)] | Sectoral privacy approach with less comprehensive protections [HIPAA, GLBA, CCPA, CPRA (State-level)] | Strongest privacy protections under GDPR with explicit customer rights | Prioritizes surveillance capabilities over individual privacy [PIPL, Cybersecurity Law] |

| Risk Categorisation | RBI enforces a three-tier KYC system (low, medium, high) to streamline onboarding | Institutions develop customized risk assessments, typically in 3-5 risk tiers (e.g., very low to very high) based on their risk appetite and customer base | The EU’s AMLDs set common risk criteria and due diligence rules to unify KYC practices across member states. No mandate on number of categories of risks. | PBOC mandates a standardized three-tier risk system (low, medium, high) aligned with national priorities |

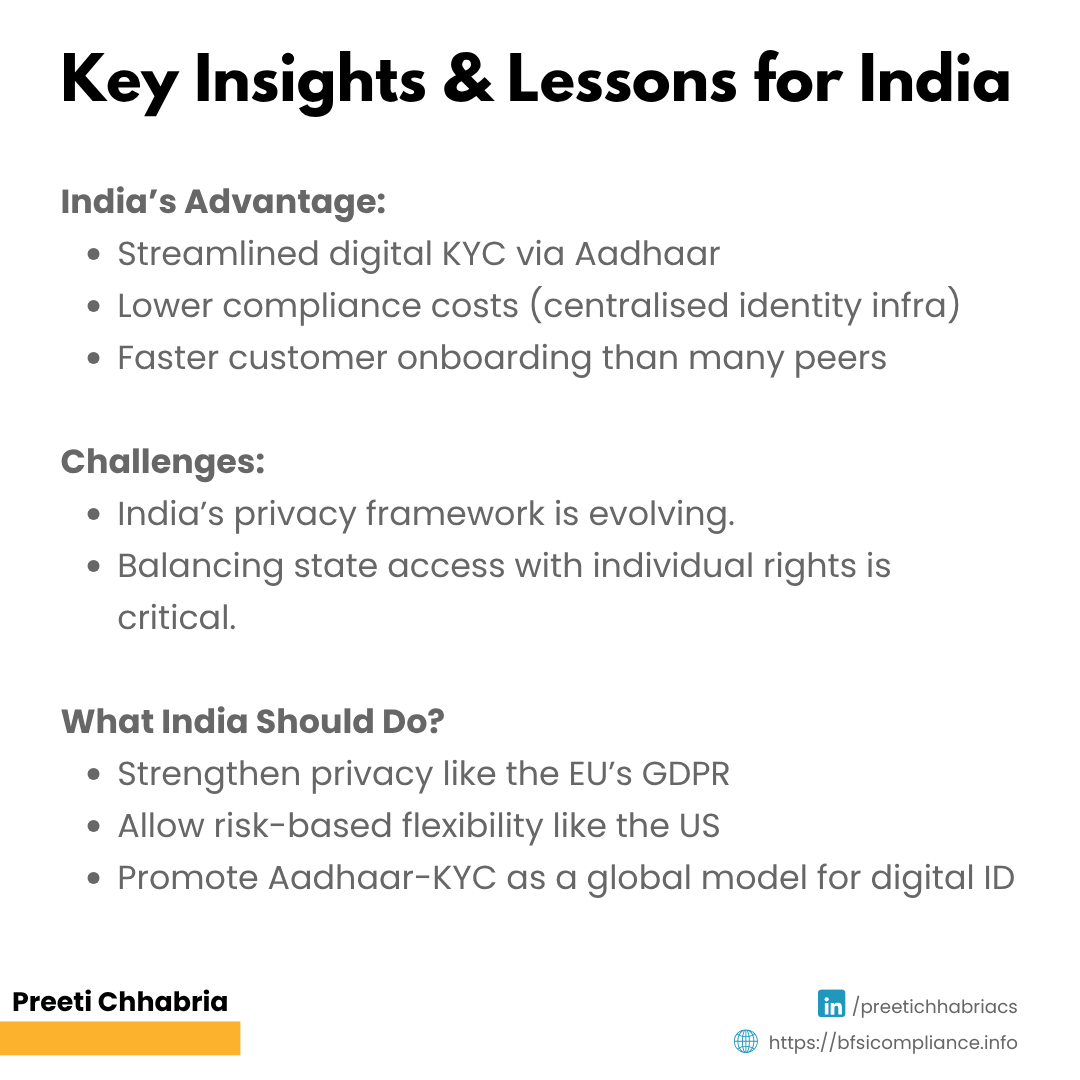

Key Insights & Lessons for India – KYC Norms

The comparative analysis reveals three distinct regulatory philosophies – non-compliance actions, privacy vs. surveillance, and risk categorisation.

The comparison reveals India’s competitive advantages:

● Streamlined digital verification

● Lower compliance costs through centralised identity infrastructure

● Faster customer onboarding

India’s evolving privacy framework must balance government access (surveillance) with individual rights (privacy). Following the EU model of explicit customer protections and leveraging our own unique biometric capabilities may be tough to achieve, but it is equally important.

These insights suggest India should:

● Strengthen privacy safeguards like the EU

● Allow greater institutional risk assessment flexibility like the US

● Position its own Aadhaar-based KYC model as a global standard for digital identity verification in financial services

Section 2: Key Features of KYC in Cryptocurrencies Across the US, EU, India and China

As digital assets reshape the financial landscape, the world needs robust KYC frameworks across countries. Unlike conventional banking, crypto transactions can be pseudonymous and cross borders instantly, requiring enhanced due diligence measures. Each major jurisdiction is developing distinct approaches to crypto KYC, reflecting their broader regulatory philosophies.

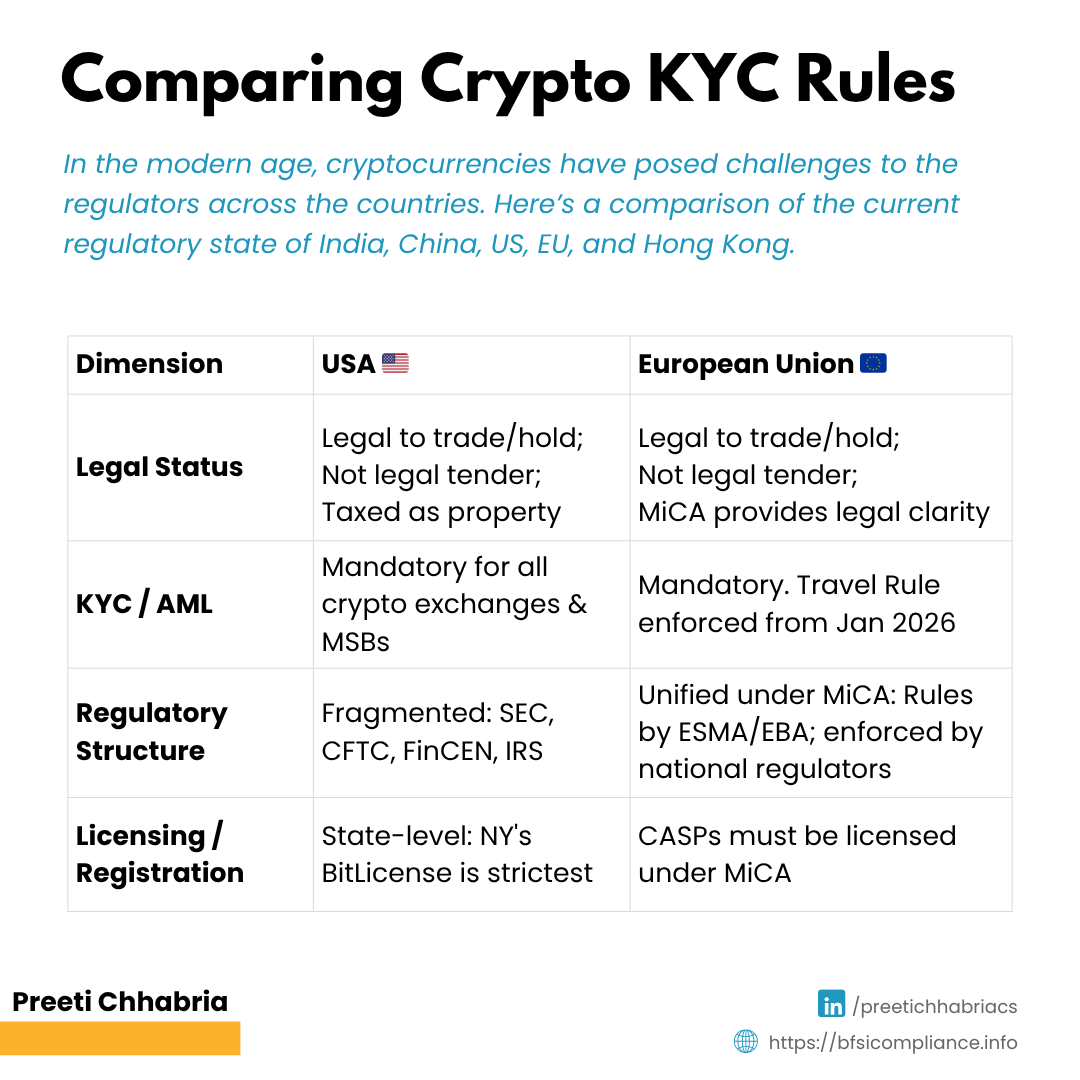

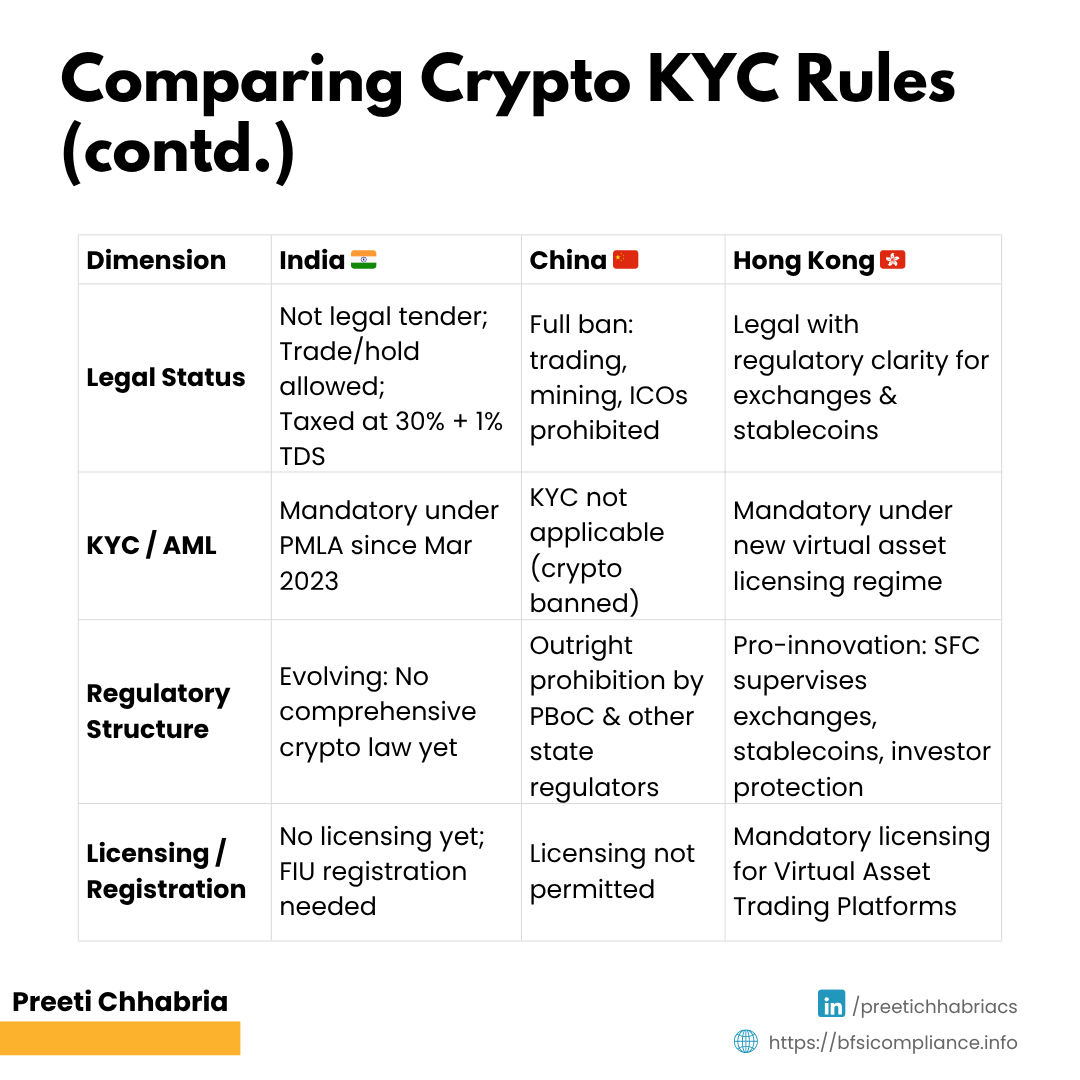

Here’s the table that summarises crypto-related laws and KYC processes for USA, EU, India, China and Hong Kong.

| Dimension | USA | European Union | India | China | Hong Kong |

|---|---|---|---|---|---|

| Legal Status of Crypto | Legal to hold and trade. Not legal tender. Taxed as property by IRS. | Legal to hold and trade. Not legal tender. Markets in Crypto-Assets (MiCA) regulations provide legal support. | Not legal tender. Holding/trading allowed. Taxed at 30% + 1% TDS. | Full ban on crypto trading, mining, ICOs. But allowed in Hong Kong. | Legal with regulation. Framework for exchanges & stablecoins. |

| KYC / AML Requirements | Mandatory for all crypto exchanges and transactions. | Mandatory. Travel Rule fully applies Jan 2026 (EU Travel Rule). | Mandatory under PMLA since March 2023. | No crypto activity allowed, so KYC doesn’t apply. | Mandatory under new licensing regime. |

| Regulatory Structure & Bodies | Fragmented: SEC (securities), CFTC (commodities), FinCEN (AML), IRS (taxes). | Country-wise separate rules, but in process to get unified via EU’s MiCA regulations. Rules by ESMA, EBA; while national regulators enforce EU MiCA. | Evolving: No single crypto law yet. Regulation via IT Dept & FIU. | Strong anti-crypto stance. PBoC & regulators implement outright ban. | Pro-innovation regulator: SFC supervises licensing, stablecoins, and investor protection. |

| Licensing / Registration | Varies by state. New York’s BitLicense is strictest. | MiCA requires CASP licensing across EU. | No licensing yet; entities must register with FIU as reporting entities under PMLA. | No licensing allowed. | Mandatory licensing for Virtual Asset Trading Platforms. |

Full Forms of Terms Used Above

IRS: Internal Revenue Service

SEC: Securities Exchange Control

CFTC: Commodity Futures Trading Commission

FinCEN: Financial Crimes Enforcement Network

ESMA: European Securities and Markets Authority

EBA: European Banking Authority

CASP: Crypto-Asset Service Provider

PMLA: Prevention of Money Laundering Act, 2002

FIU: Financial Intelligence Unit

ICOs: Initial Coin Offering

PBOC: People’s Bank of China

SFC: Securities and Futures Commission

Conclusion

KYC regulations across the globe exhibit diverse philosophies, yet all strive to combat illicit financial activities. With cryptocurrencies opening new frontiers in the world of finance, it has become more difficult to ensure legitimacy and transparency in the business. The overarching trend points towards more rigorous due diligence. But we see a divergence in the crypto space – the EU moves towards comprehensive standardisation, the US maintains a fragmented approach, India is in the grey zone, while China enforces an outright ban.

For India, the path forward must include leveraging Aadhaar infrastructure, strengthening privacy laws, fostering innovation and bringing comprehensive crypto regulations in place.