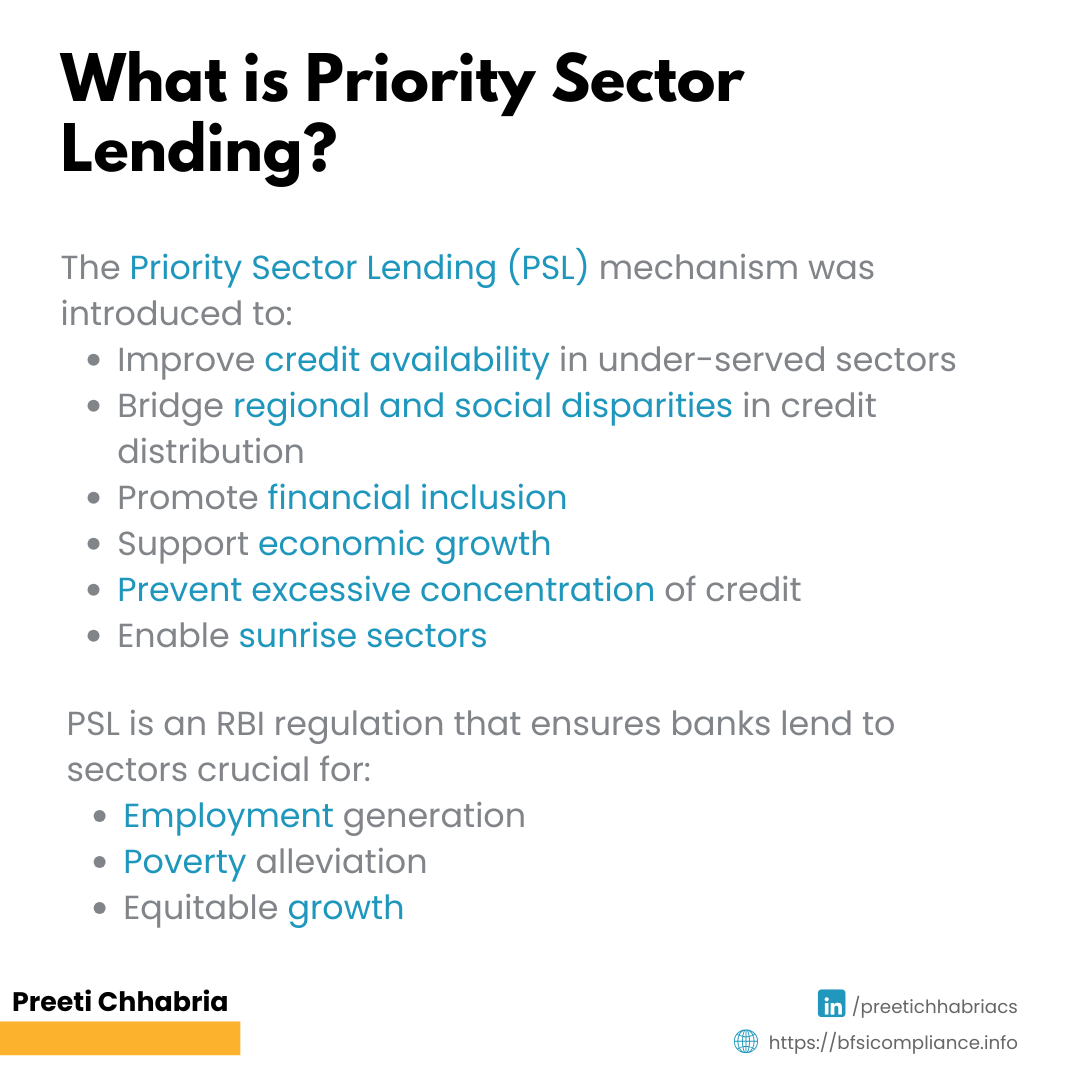

Priority sector lending (PSL) is a regulatory framework that ensures specific sectors in the economy get extra attention. Banks must lend to these sectors without fail. These sectors are important in terms of employment generation, poverty alleviation, and equitable growth.

Significance of PSL

The PSL mechanism was introduced to:

● Improve credit availability in under-served sectors like agriculture, MSMEs, and weaker sections of society.

● Bridge regional and social disparities in credit distribution.

● Promote financial inclusion and support economic activities that have a high social return but may be commercially less attractive.

● Prevent excessive concentration of credit in certain industries or geographies.

● Enable sunrise sectors like renewable energy.

Categories under Priority Sector

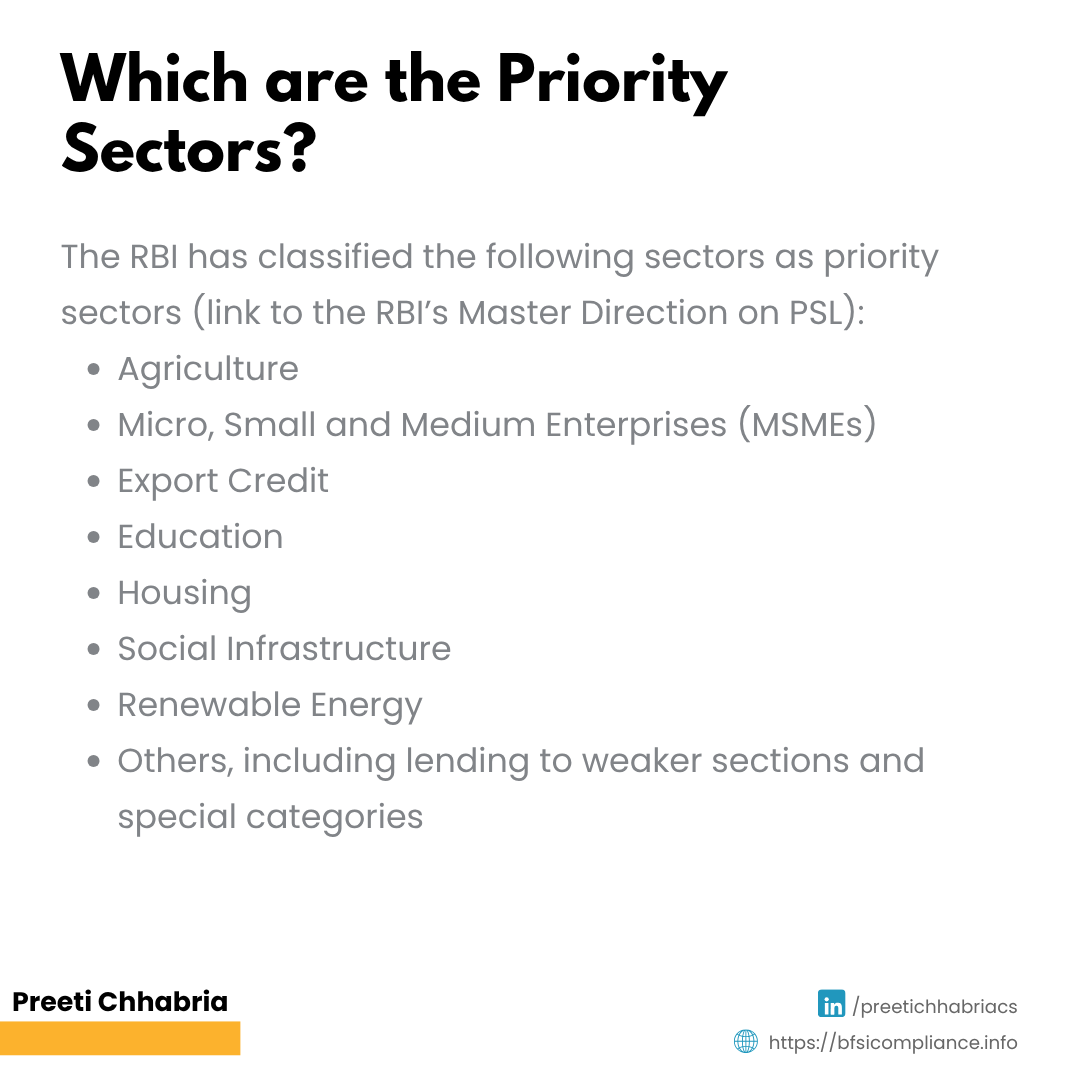

The RBI has classified the following sectors as priority sectors (link to the RBI’s Master Direction on PSL):

● Agriculture

● Micro, Small and Medium Enterprises (MSMEs)

● Export Credit

● Education

● Housing

● Social Infrastructure

● Renewable Energy

● Others, including lending to weaker sections and special categories

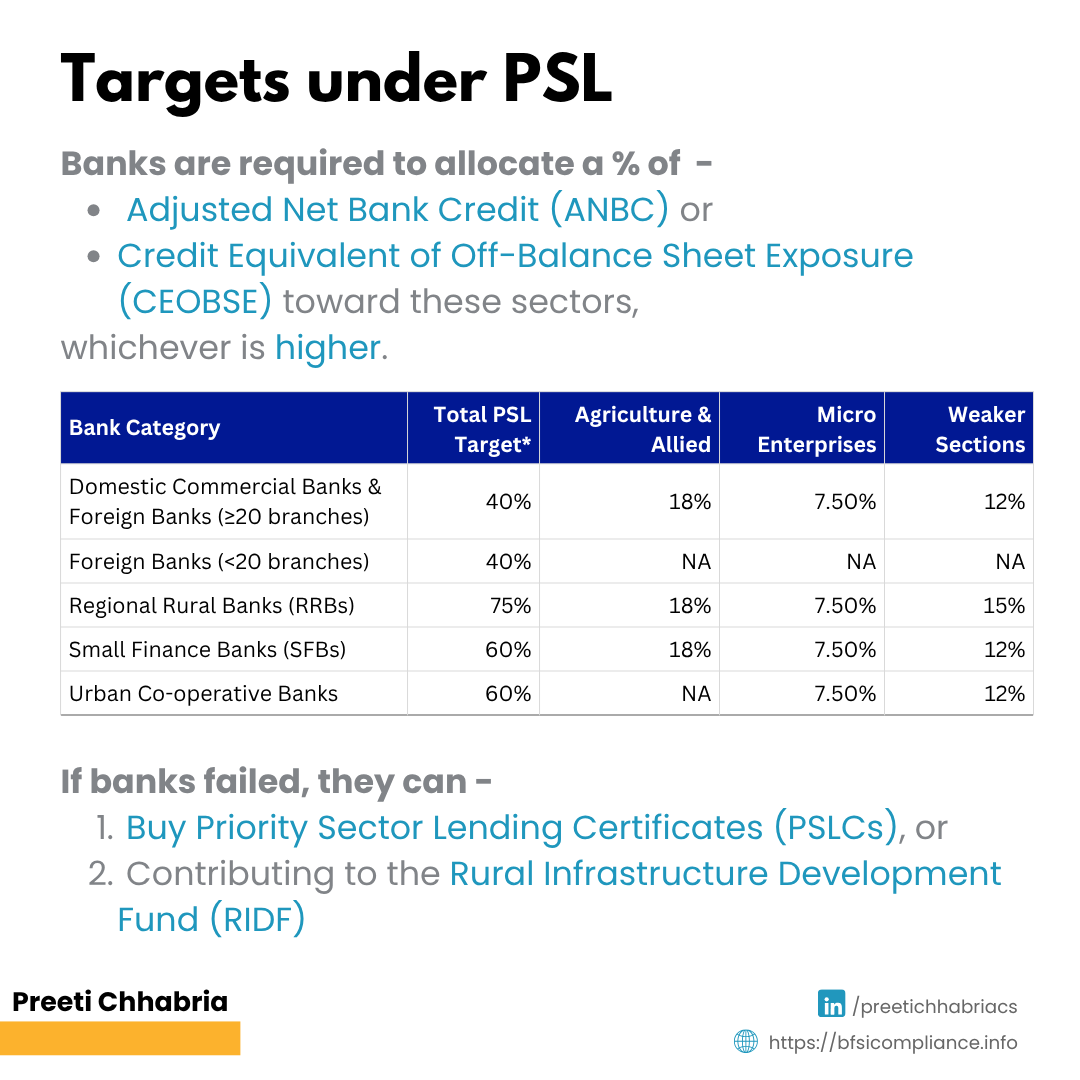

Targets under PSL

Banks are required to allocate a portion of their Adjusted Net Bank Credit (ANBC) or Credit Equivalent of Off-Balance Sheet Exposure (CEOBSE) toward these sectors, whichever is higher.

What if Banks Fail to Comply?

But what if a bank falls short of the targets? There are two ways in which this is dealt with:

1. Buying Priority Sector Lending Certificates (PSLC)

If a bank falls short, it can buy Priority Sector Lending Certificates (PSLCs) from another bank that has lent more than required. These certificates don’t involve any transfer of actual loans or risk.

There are four types of PSLCs: agriculture, small/marginal farmers, micro enterprises, and general priority lending. Each type counts toward different targets.

PSLCs are traded on the RBI’s e-Kuber platform. Banks can even sell some PSLCs without holding the actual loans, but by year-end (March 31), they must meet their targets through a mix of actual lending and net PSLCs. The certificates expire on March 31.

Here are the two illustrations:

1. Bank A may sell PSLCs with a nominal value of Rs. 100 crores to Bank B on July 15, 2025. Bank B can then recognise Rs. 100 crore towards its PSL target for the reporting dates of September 30, 2025, December 31, 2025 & March 31, 2026. Bank A will subtract the same from its achievement figures for the respective reporting dates. The PSLC will expire by March 31, 2026.

2. Bank C may buy Rs. 100 crore PSLC on March 30, 2017, from Bank D and achieve its target. Bank D will subtract Rs. 100 crore from its PSL reporting on March 31, 2026. The PSLC will expire by March 31, 2026.

2. Contributing to the Rural Infrastructure Development Fund (RIDF)

All banks (except certain Urban Cooperative Banks) that don’t meet their PSL targets will have to put money into special funds like the Rural Infrastructure Development Fund (RIDF) or others managed by NABARD, NHB, SIDBI, or MUDRA Ltd., as decided by the RBI.

This mechanism ensures that even when banks fall short, funds still reach priority sectors.

Banks get interest on such contributions or deposits, but not at the market rate. Here’s the calculation:

● <5 percentage points (ppt) shortfall: Interest = Bank rate minus 2ppt

● 5–10 ppt: Bank rate minus 3ppt

● 10+ ppt: Bank rate minus 4ppt

● If the overall target is met, but the sub-sector target is not met: Bank rate minus 2ppt

This acts as an indirect penalty for banks, since the money parked in these funds earns lower returns compared to what they could have earned if they had met their targets by actually lending.

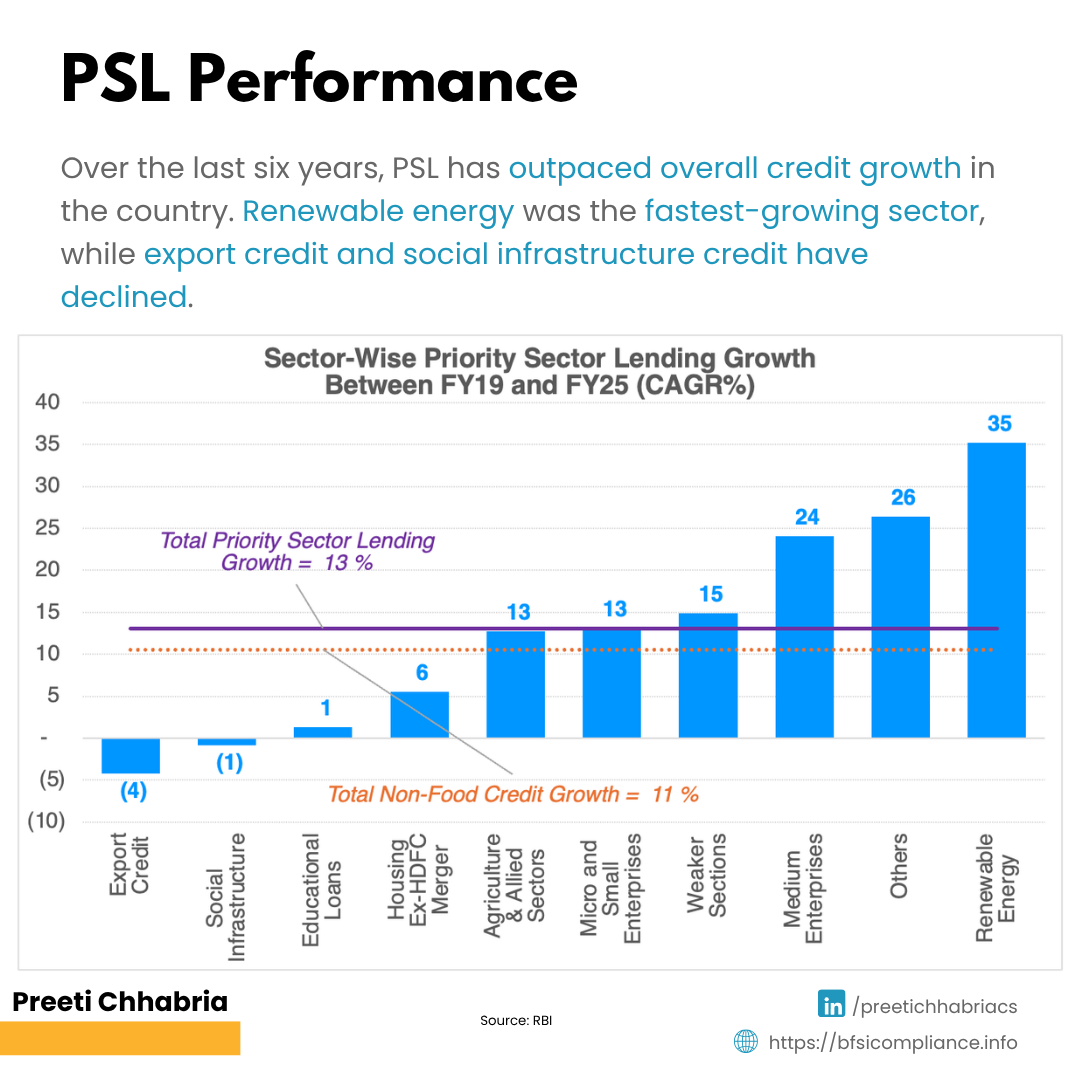

PSL Performance

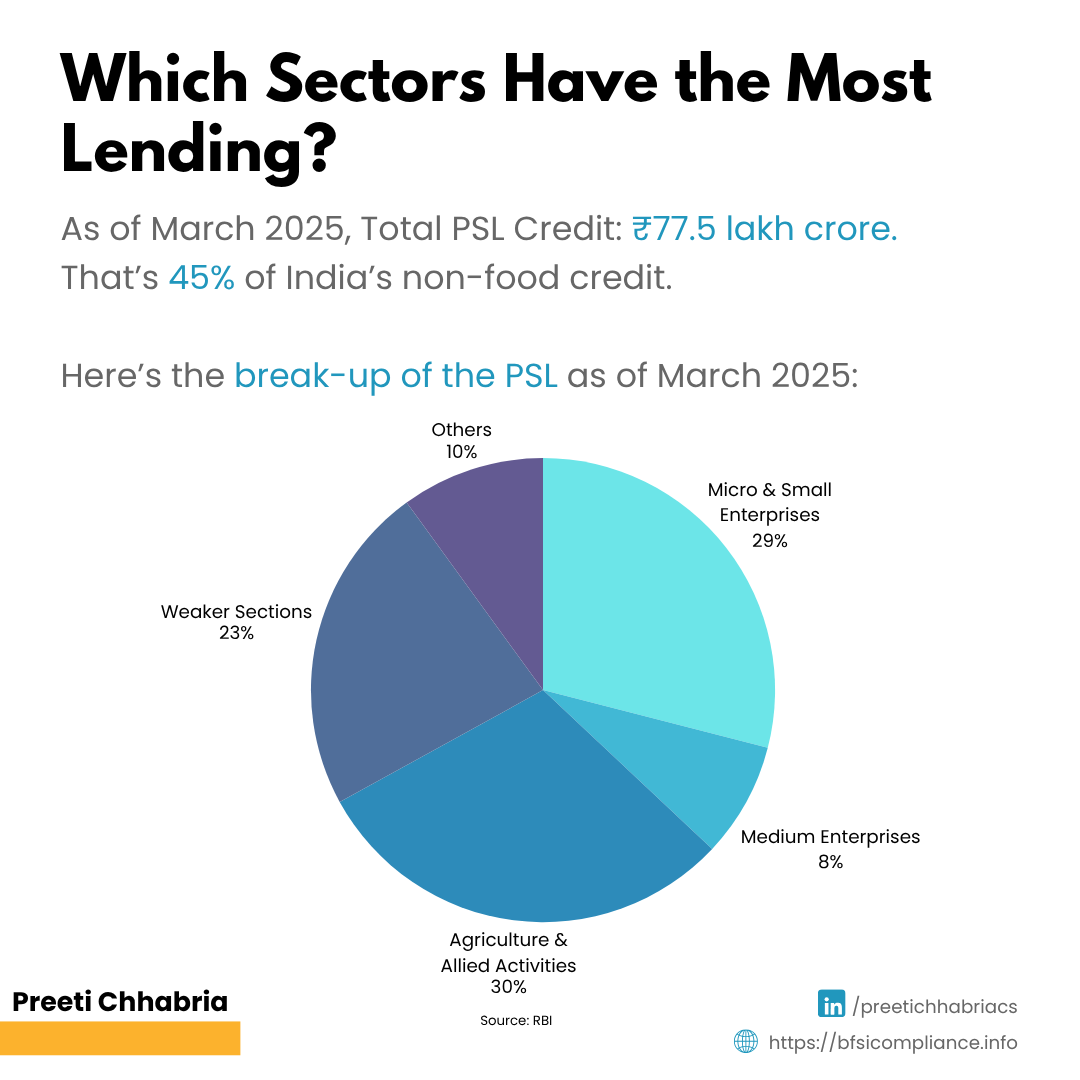

As of March 2025, total outstanding credit under PSL stood at Rs. 77.5 lakh crore, accounting for nearly 45% of India’s total non-food credit, more than the 40% requirement. This reflects the strong role PSL continues to play in driving inclusive credit growth across key sectors of the economy.

A closer look at the composition shows that three categories dominate:

● MSMEs: 37% [micro & small 29% + medium enterprises 8%]

● Agriculture and allied activities: 30%

● Weaker sections: 23%

Source: RBI

Over the last six years, PSL has outpaced overall credit growth in the country. PSL credit has grown by 13% CAGR, whereas total non-food credit grew by 11% CAGR.

However, the growth has been uneven across the sub-sectors. Renewable energy was the fastest-growing sector, considering the government’s push for cleaner energy alternatives. It grew by 35% CAGR between FY19 and FY25. It was followed by lending to medium enterprises (24%).

Sectors like agriculture (13%), micro & small enterprises (13%) and weaker sections (15%) have seen steady growth rates – at par with the overall growth rates.

However, export credit (-4%) and social infrastructure credit (-1%) have declined. On the other hand, education loans (1%) remained flat while housing loans have seen a mere 6% growth.

Data Source: RBI Database – Sectoral Deployment of Non-Food Gross Bank Credit – Outstanding