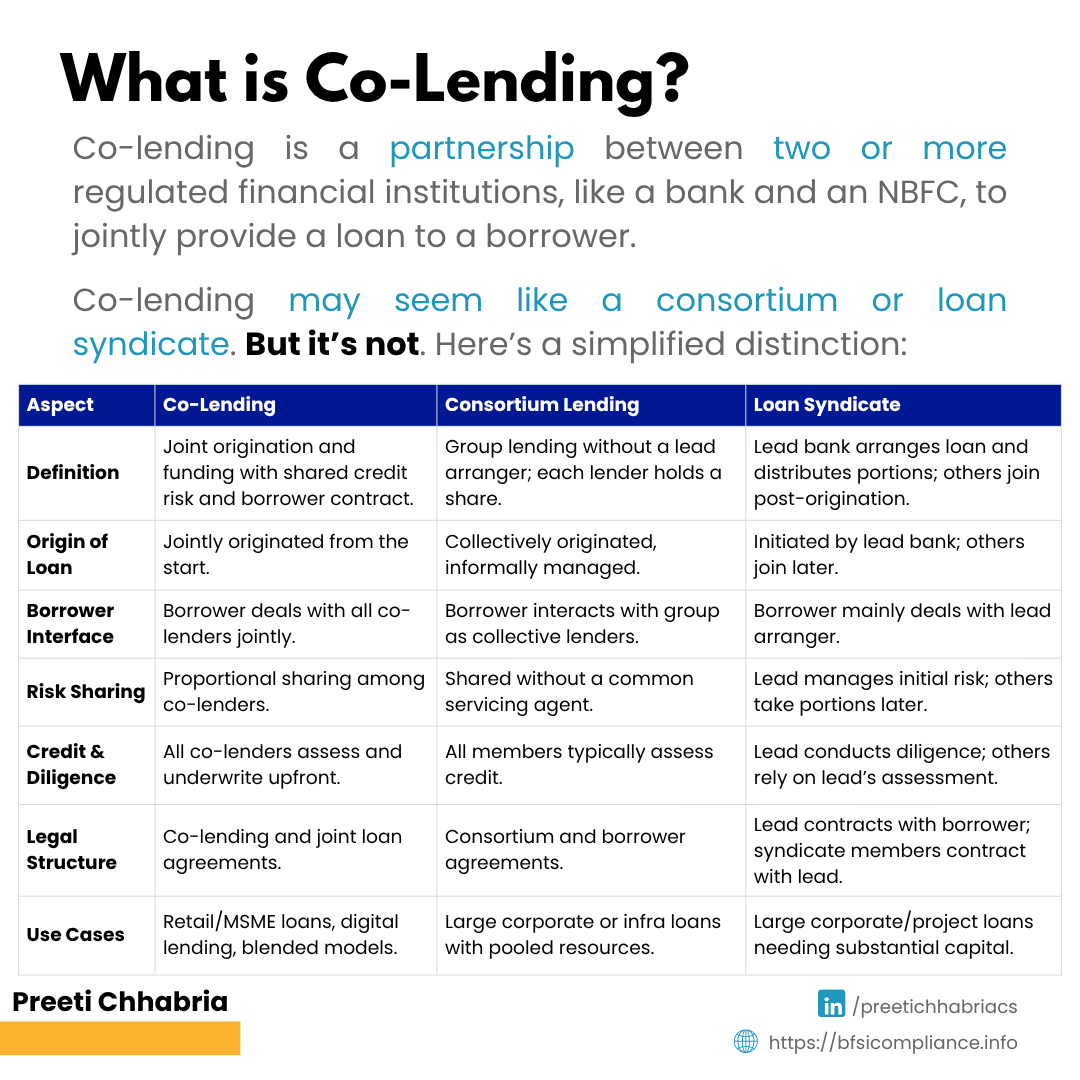

What is Co-Lending?

Co-lending is a partnership between two or more regulated financial institutions, like a bank and an NBFC, to jointly provide a loan to a borrower. They agree on how much each will contribute and then share the profits and risks proportionally.

Co-lending may seem like a consortium or loan syndicate. But it’s not. Here’s a simplified distinction between these three forms of lending:

Comparison: Co-Lending vs Consortium Lending vs Loan Syndicate

| Aspect | Co-Lending | Consortium Lending | Loan Syndicate |

|---|---|---|---|

| Definition | A horizontal partnership where lenders jointly originate and fund a loan, sharing credit risk and rewards directly from the start, with joint contractual obligations to the borrower. | A group of lenders jointly lend to a borrower, often for large corporate loans, each responsible for a share, but lend collectively without a lead arranger managing the group. | A loan arranged by a lead bank or financial institution, which then distributes portions to syndicate members; syndicate members usually do not participate in origination or borrower interface. |

| Origin of Loan | Jointly originated by all co-lenders at inception. | Typically collectively arranged and managed. | Origination is done by lead bank; syndicate members join after loan origination. |

| Borrower Interface | Borrower deals jointly with all co-lenders as joint promisees. | Borrower interacts with consortium as a group; legally all are lenders. | Borrower mainly interfaces with lead arranger; contract mainly with the lead bank. |

| Risk Sharing | Risk and rewards are proportionally shared among all co-lenders. | Shared among consortium members. | Lead manages initial risk; syndicate members take assigned portions. |

| Credit & Due Diligence | All co-lenders involved upfront. | Generally all members participate. | Lead bank performs due diligence; others rely on it. |

| Legal Structure | Co-lending agreement + joint loan agreement. | Consortium agreement + loan agreement. | Agreements primarily with lead arranger. |

| Common Use Cases | Retail, MSME loans, blended expertise models, digital lending partnerships. | Large corporate or infrastructure financing. | Large corporate/project loans. |

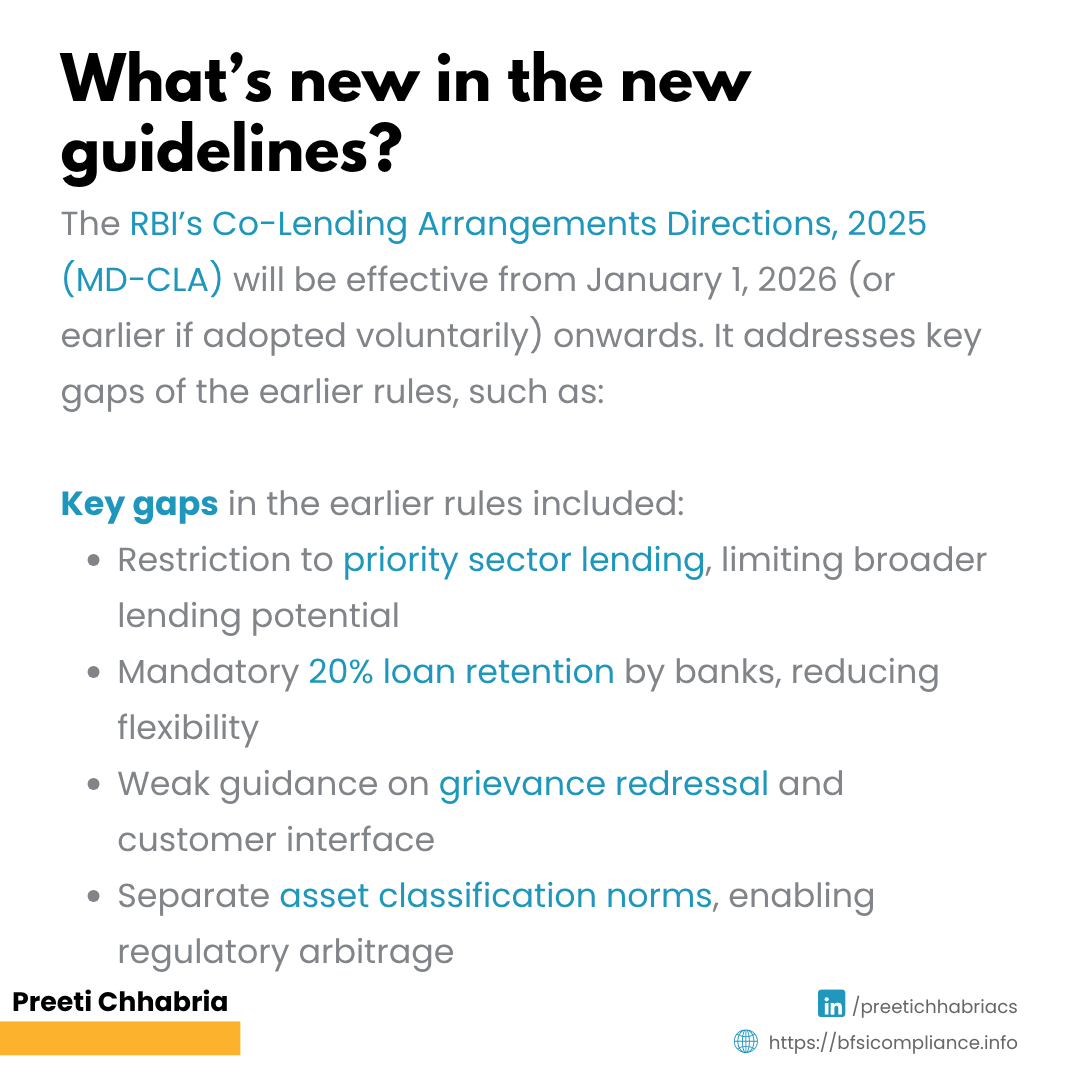

The New Guidelines

The Reserve Bank of India (RBI) has released the Co-Lending Arrangements Directions, 2025 (MD-CLA), a landmark framework that redefines co-lending in India. The framework comes into effect on January 1, 2026 (or earlier if adopted voluntarily).

Why Were the Previous Guidelines Insufficient?

Unlike the earlier 2020 guidelines—which were limited to priority sector lending (PSL)—the new rules expand the framework to all lending activities while strengthening risk management, transparency, and borrower protection.

The earlier framework had gaps such as:

It applied only to PSL, limiting scope outside mandated lending

Required banks to retain at least 20% of every loan, reducing flexibility

Limited guidance on grievance redressal, transparency, and customer interface

Separate asset classification norms created regulatory arbitrage

The new guidelines address these issues and create a more comprehensive, borrower-centric, and operationally robust regime.

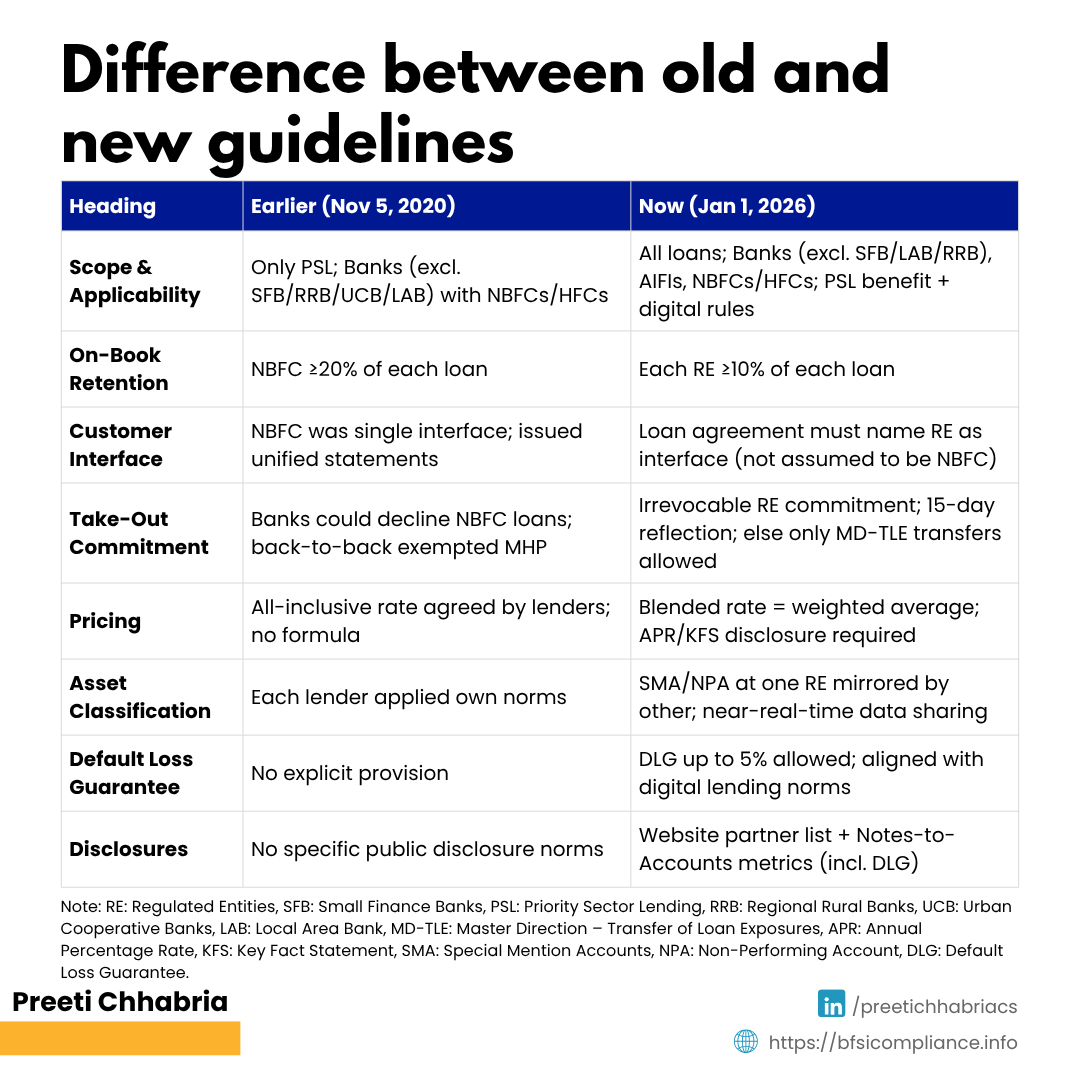

What Changed vs November 5, 2020 Circular?

| Heading | Earlier (Nov 5, 2020) | Now (Jan 1, 2026) |

|---|---|---|

| Scope & Applicability | Only PSL; Banks (excl. SFB/RRB/UCB/LAB) with NBFCs/HFCs | All loans; Banks (excl. SFB/LAB/RRB), AIFIs, NBFCs/HFCs. PSL benefit continues. Digital lending rules apply where relevant. |

| Minimum on-book retention | NBFC ≥20% of each loan | Each RE ≥10% of each loan |

| Customer interface | NBFC was single point of interface and issued unified statements | Loan agreement must name RE as single interface (not presupposed as NBFC) |

| Take-out commitment & timing | Banks could decline NBFC-originated loans; back-to-back clauses exempt MHP | Irrevocable commitment required; 15-day on-book reflection; fallback to MD-TLE transfers |

| Pricing | All-inclusive borrower rate agreed by lenders | Blended interest rate (weighted average); APR/KFS disclosure required |

| Asset classification | Each lender applied own classification/provisioning | SMA/NPA mirrored across REs; near-real-time data sharing |

| Default Loss Guarantee (DLG) | Not specified | DLG up to 5% allowed (originator), aligned with digital lending framework |

| Disclosures | No structured disclosure framework | Website partner list + Notes-to-Accounts metrics (incl. DLG) |

Benefits of the New Framework

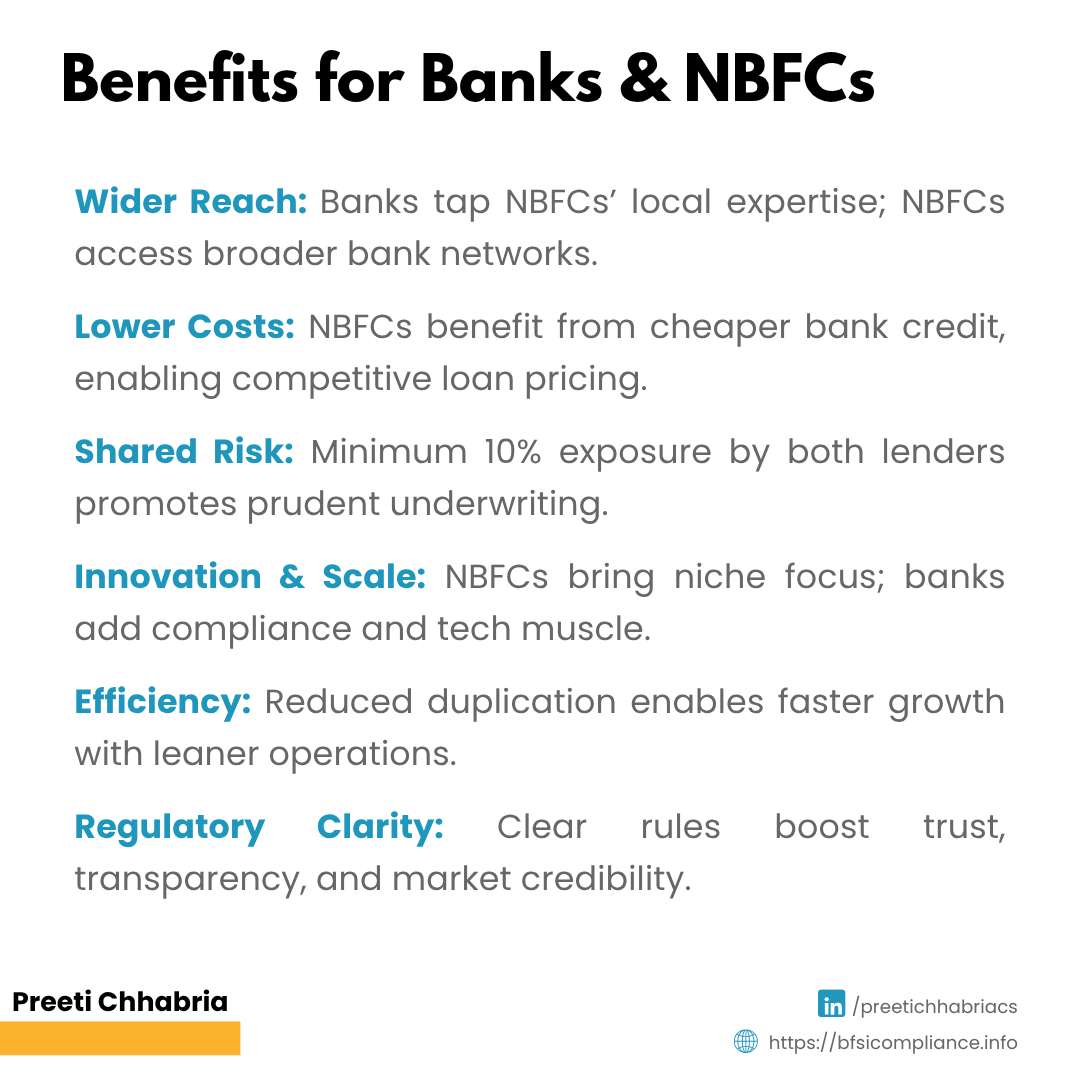

For Banks & NBFCs

Wider reach and market expansion through partnerships

Lower funding costs for NBFCs via bank credit access

Shared risk with minimum exposure requirement

Product innovation through combined strengths

Operational efficiency and faster scaling

Greater regulatory clarity and credibility

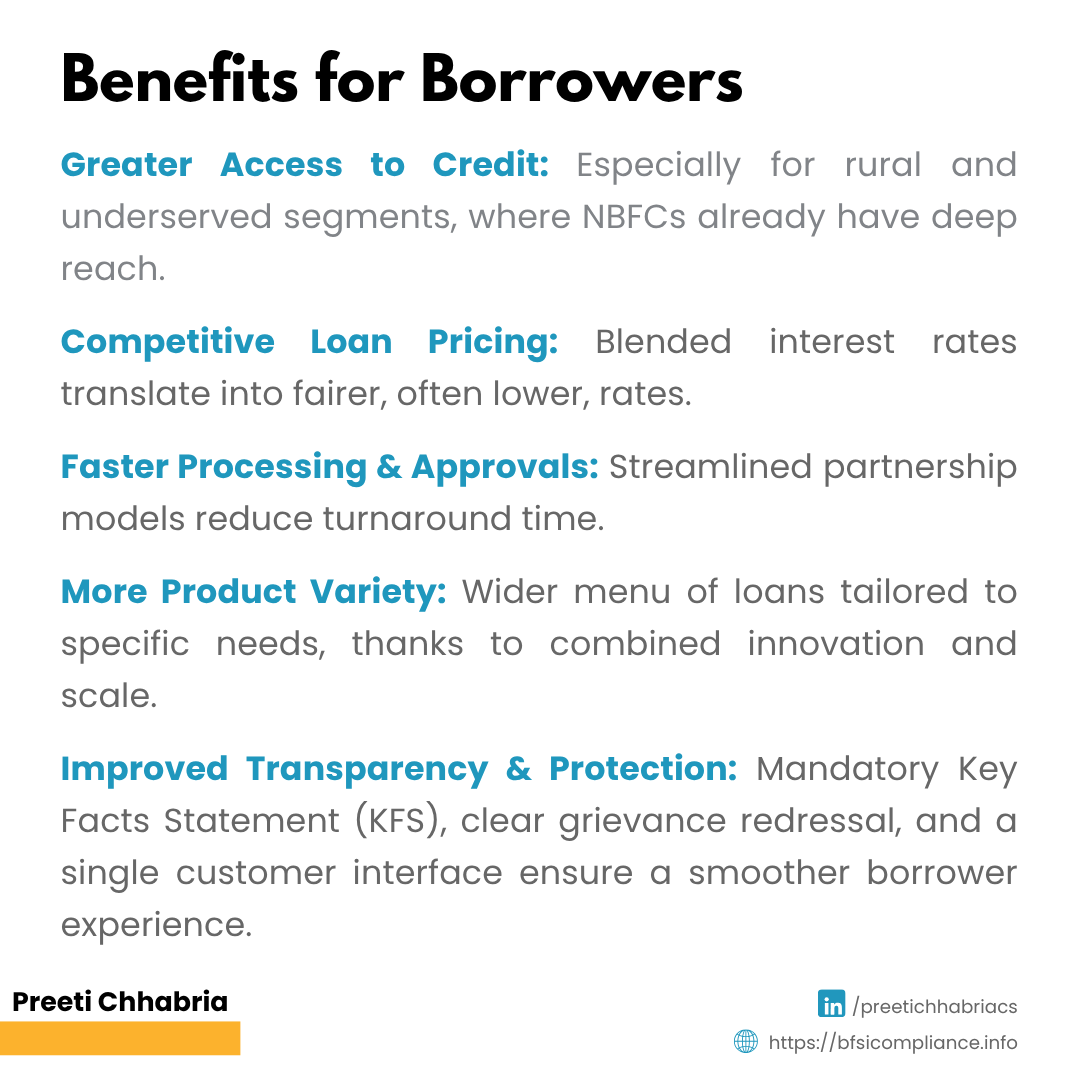

For Borrowers

Improved access to credit, especially underserved segments

More competitive pricing through blended rates

Faster processing and approvals

Greater product variety and customization

Higher transparency through KFS and grievance redressal mechanisms

Conclusion

The 2025 co-lending guidelines mark a major policy upgrade by RBI, expanding co-lending from a narrow PSL-focused model into a comprehensive credit delivery framework.