The Reserve Bank of India has now issued the Credit Information Reporting Amendment Directions, 2025, bringing changes to the credit reporting framework released earlier this year. These amendments, notified on December 4, 2025, refine several operational aspects of credit information reporting.

For the details on the master directions, refer to Newsletter #4 titled “RBI’s New Credit Reporting Guidelines: What You Need to Know?”

While the original directions introduced a credit reporting regime, this amendment focuses on the frequency, accuracy, and timeliness of data. In other words, the previous newsletter article (Part 1) discusses the basic principles and foundations, while this piece (Part 2) discusses the operational changes introduced in December 2025.

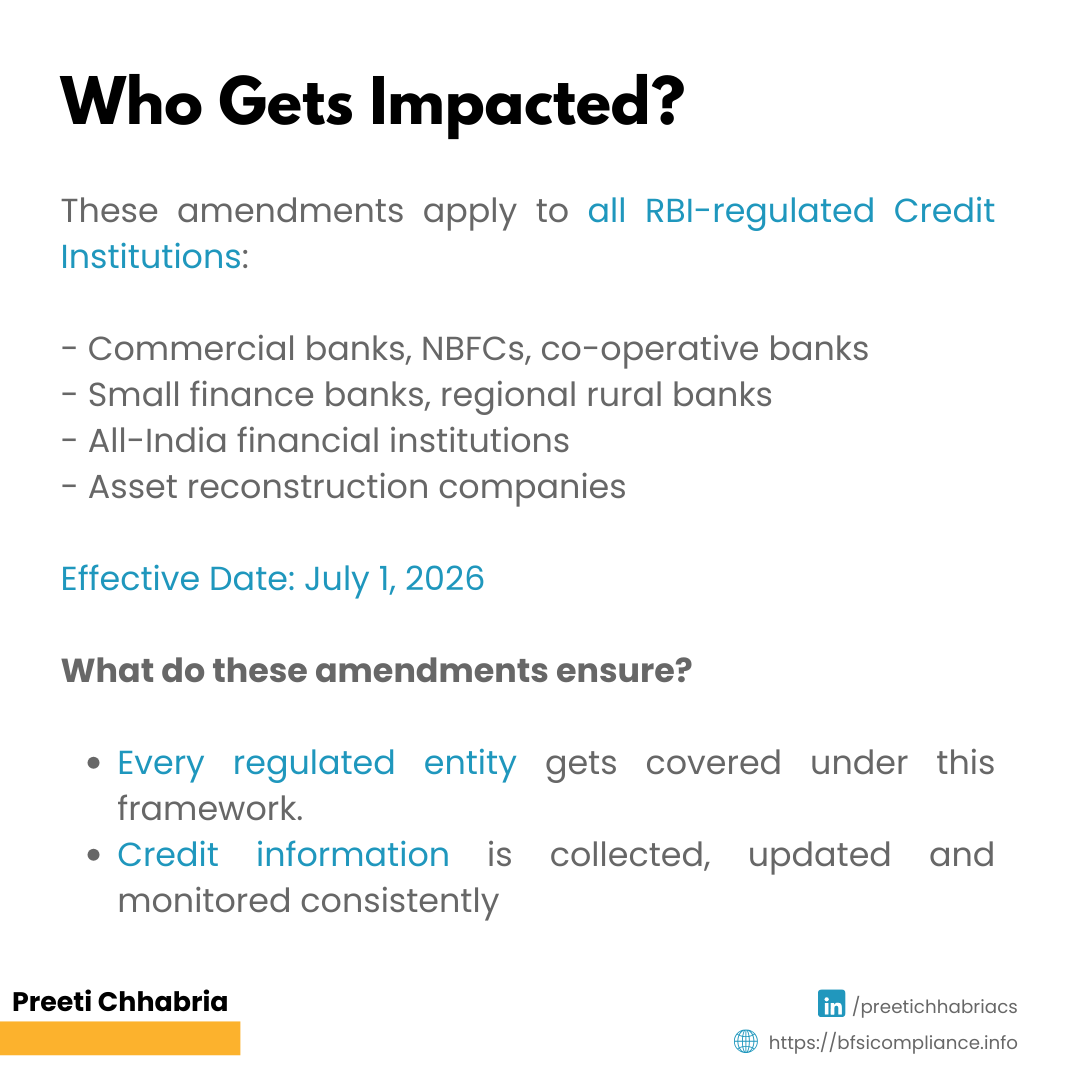

Who Gets Impacted by These Amendments?

These credit reporting amendments apply uniformly to all RBI-regulated Credit Institutions — including:

- Commercial banks

- NBFCs

- Co-operative banks

- Small finance banks

- Regional rural banks

- All-India financial institutions

- Asset reconstruction companies

In effect, every regulated lender that reports borrower data to credit bureaus is covered under this framework. This ensures that credit information is collected, updated, and monitored consistently across the entire lending ecosystem.

The amended rules will come into force from July 1, 2026. Here’s what has changed:

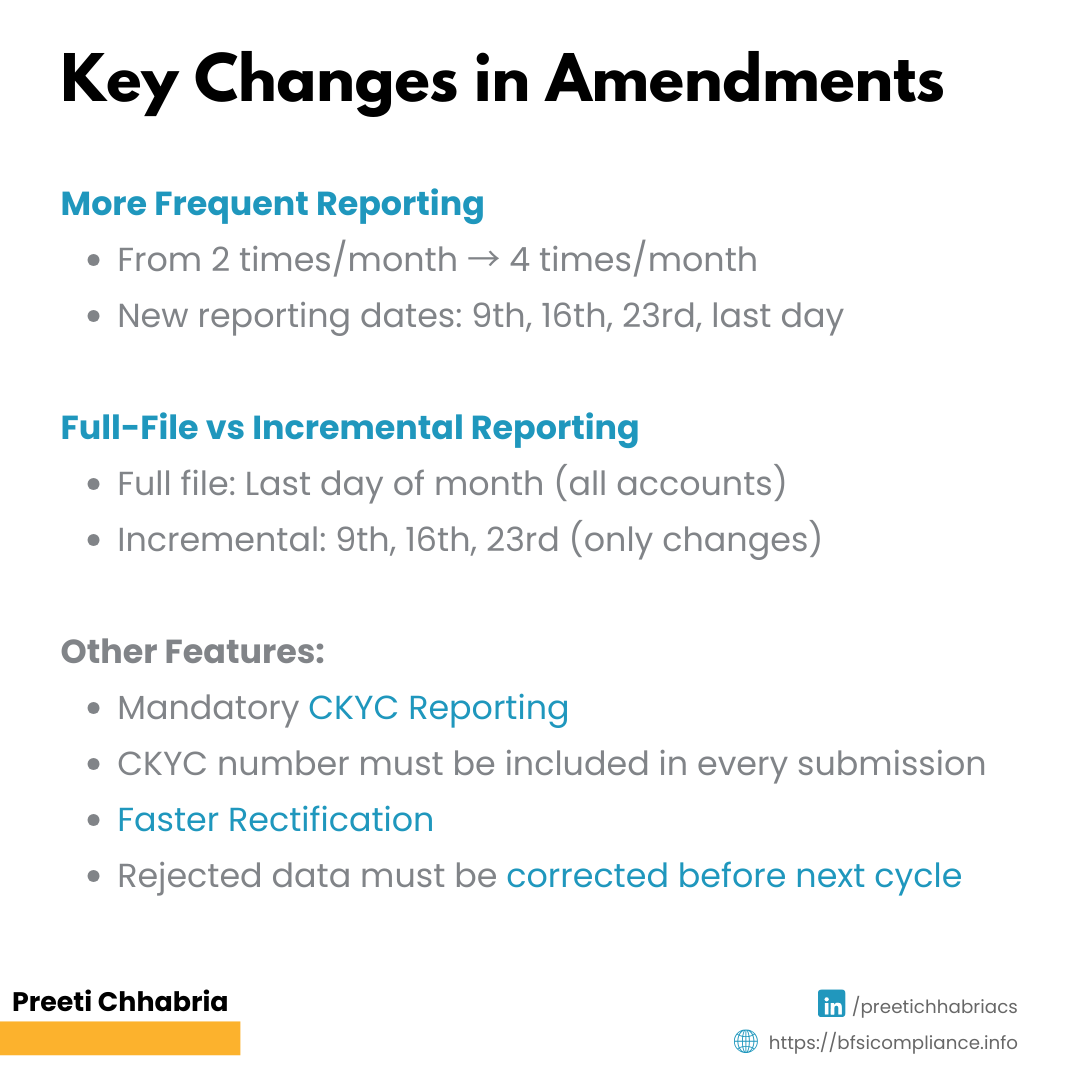

More Frequent Reporting by Credit Institutions

Under the original directions, credit institutions were required to update borrower information twice a month — on the 15th and the last day — and transmit it to credit bureaus within seven days.

The new amendment introduces four mandatory reporting dates each month:

- 9th

- 16th

- 23rd

- Last day of the month

This means borrower data will now be refreshed almost weekly. This gives lenders more up-to-date information for risk assessment. In short, the ecosystem is moving toward near-real-time reporting.

Full-File and Incremental-File Structure

Since there are four reporting dates under the new rules, RBI has introduced a structured reporting approach to reduce compliance burden.

Full File Reporting

Credit institutions must submit a complete dataset — called full file reporting — once every month on the last day.

- Covers all active accounts

- Includes all closed accounts since the last report

- Must reach credit bureaus by the 5th of the following month

Incremental File Reporting

For the other three dates (9th, 16th, 23rd), institutions must submit only incremental reports, which include:

- New accounts

- Closed accounts

- Accounts with changes

- Accounts that have become overdue

- Changes in days past due (DPD)

These reports must be submitted within four days.

Mandatory CKYC Number Reporting

Credit institutions must now include the borrower’s CKYC number in every submission to credit bureaus.

- For new borrowers, CKYC must be updated once generated

- This improves identity accuracy

- Reduces duplication

- Enhances credit profile matching across lenders

Faster Rectification Process

Previously, correction timelines were broad and less defined.

Now:

- Any rejected or incorrect data must be corrected

- Resubmission must happen before or along with the next reporting cycle

This ensures that discrepancies do not persist in borrower credit histories.

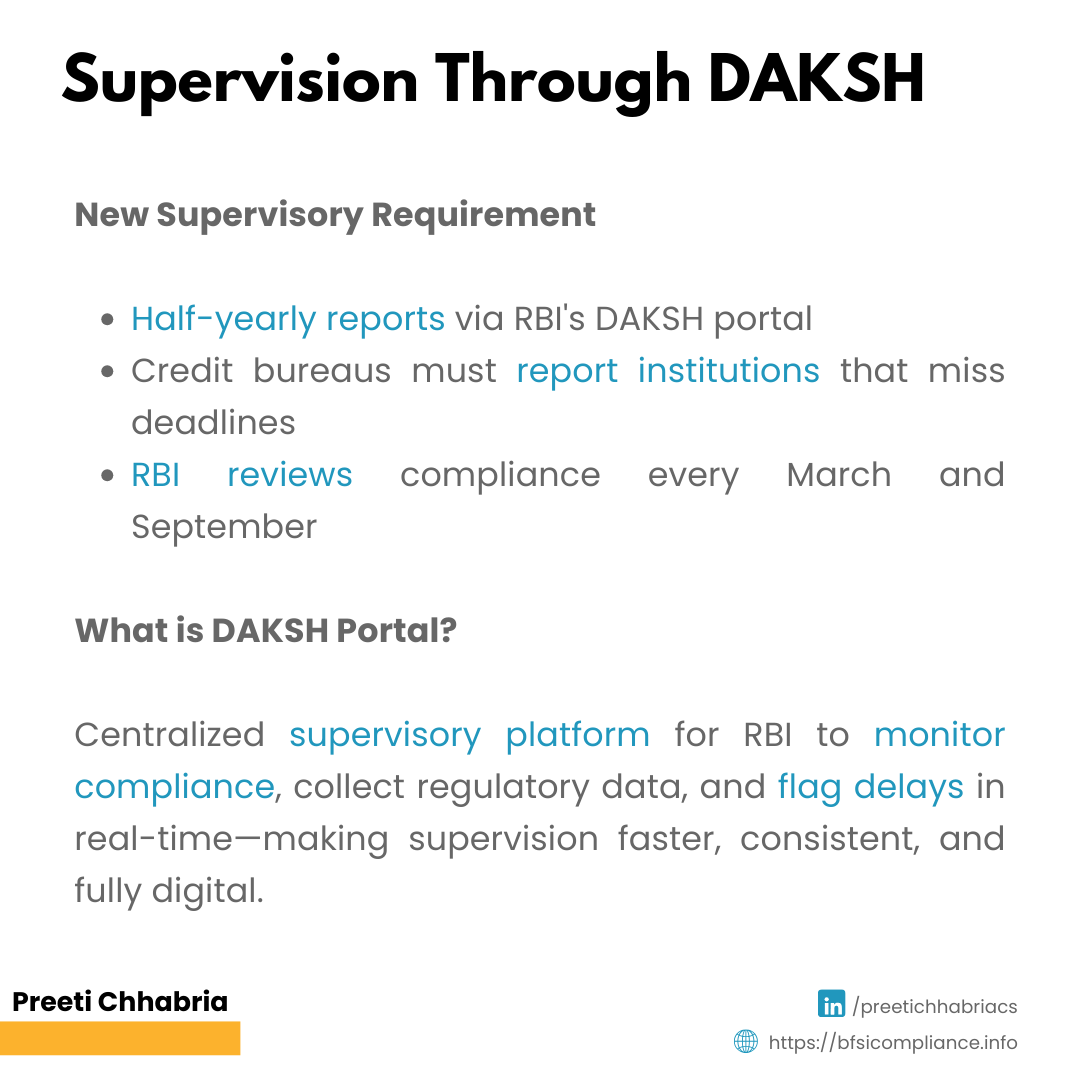

Supervision Through DAKSH

A new supervisory requirement mandates half-yearly reporting via the RBI’s DAKSH portal*.

- Credit Information Companies must report institutions missing deadlines

- RBI’s Department of Supervision will review cases in March and September

This strengthens monitoring of reporting delays and compliance behaviour.

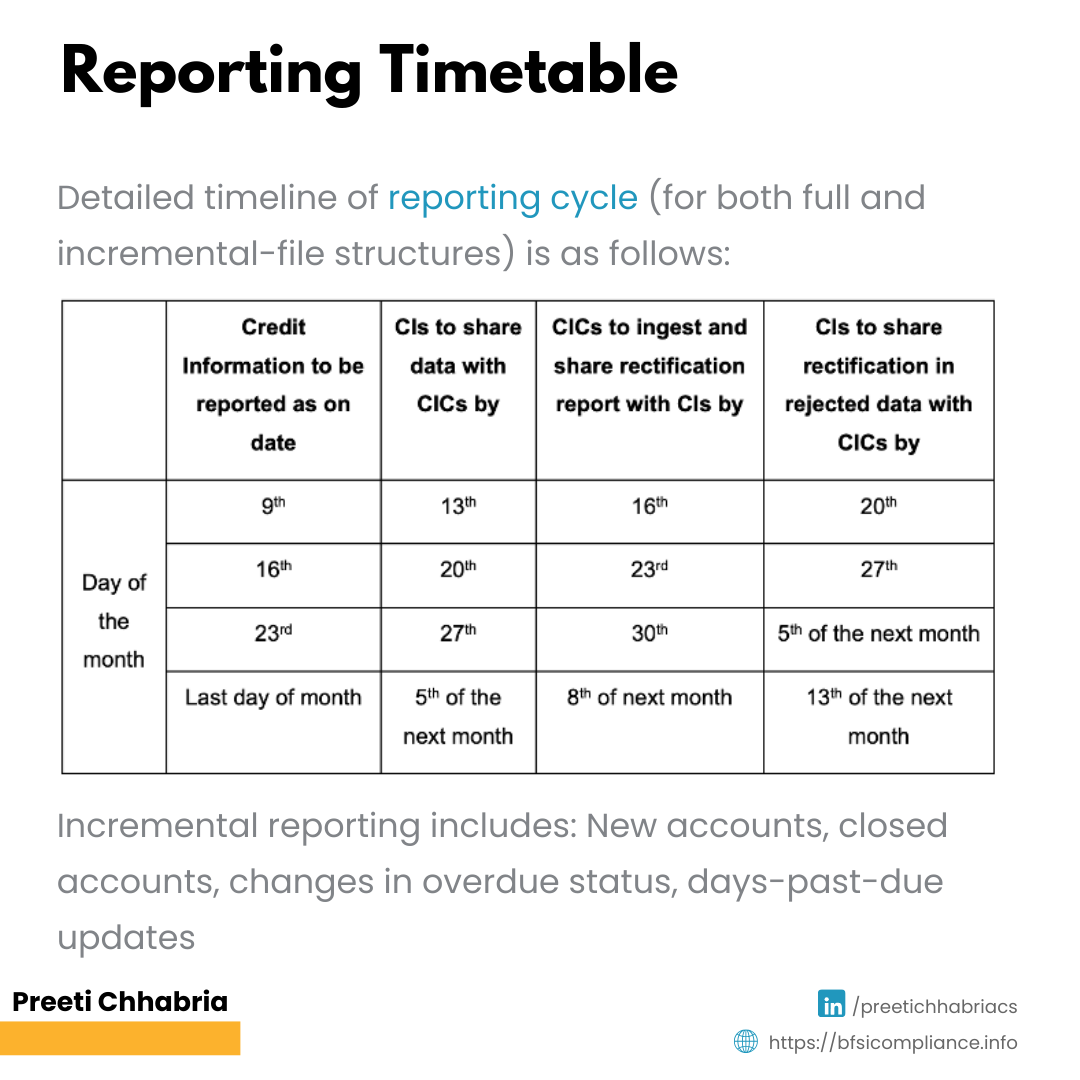

Defined Timelines for Data Flow

The amendment includes an annexure that provides a detailed timeline for the reporting cycle (full and incremental file structures). This gives operational clarity and improves efficiency in execution.

Final Take

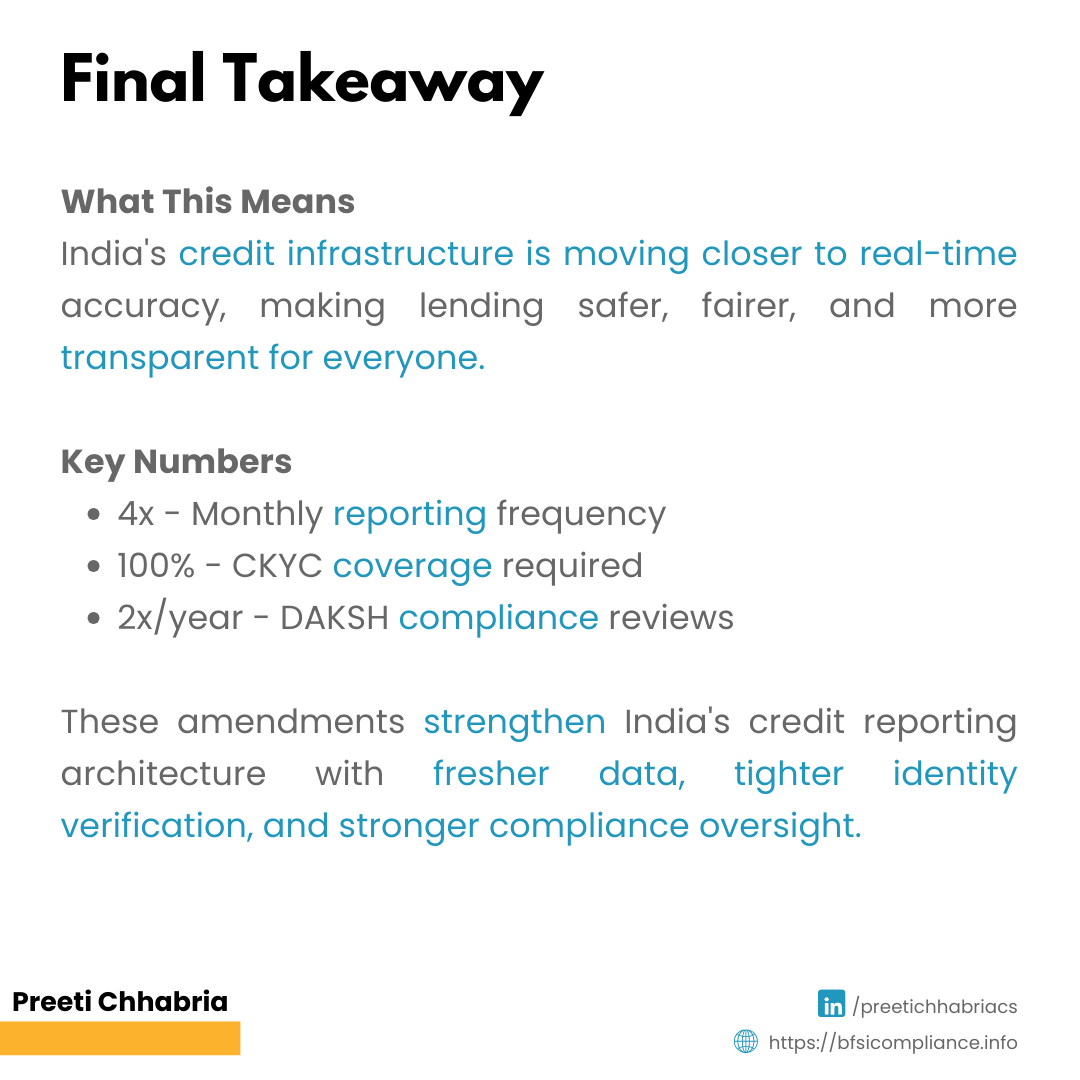

Taken together, these amendments significantly strengthen India’s credit reporting architecture.

Moving to four reporting cycles a month ensures lenders work with more current data, improving early stress detection and risk assessment. The distinction between full-file and incremental-file reporting improves efficiency without compromising accuracy. Mandatory CKYC integration enhances identity verification, while stricter rectification timelines ensure errors do not persist in the system. Continuous oversight through the DAKSH platform reinforces compliance discipline across lenders and credit bureaus.

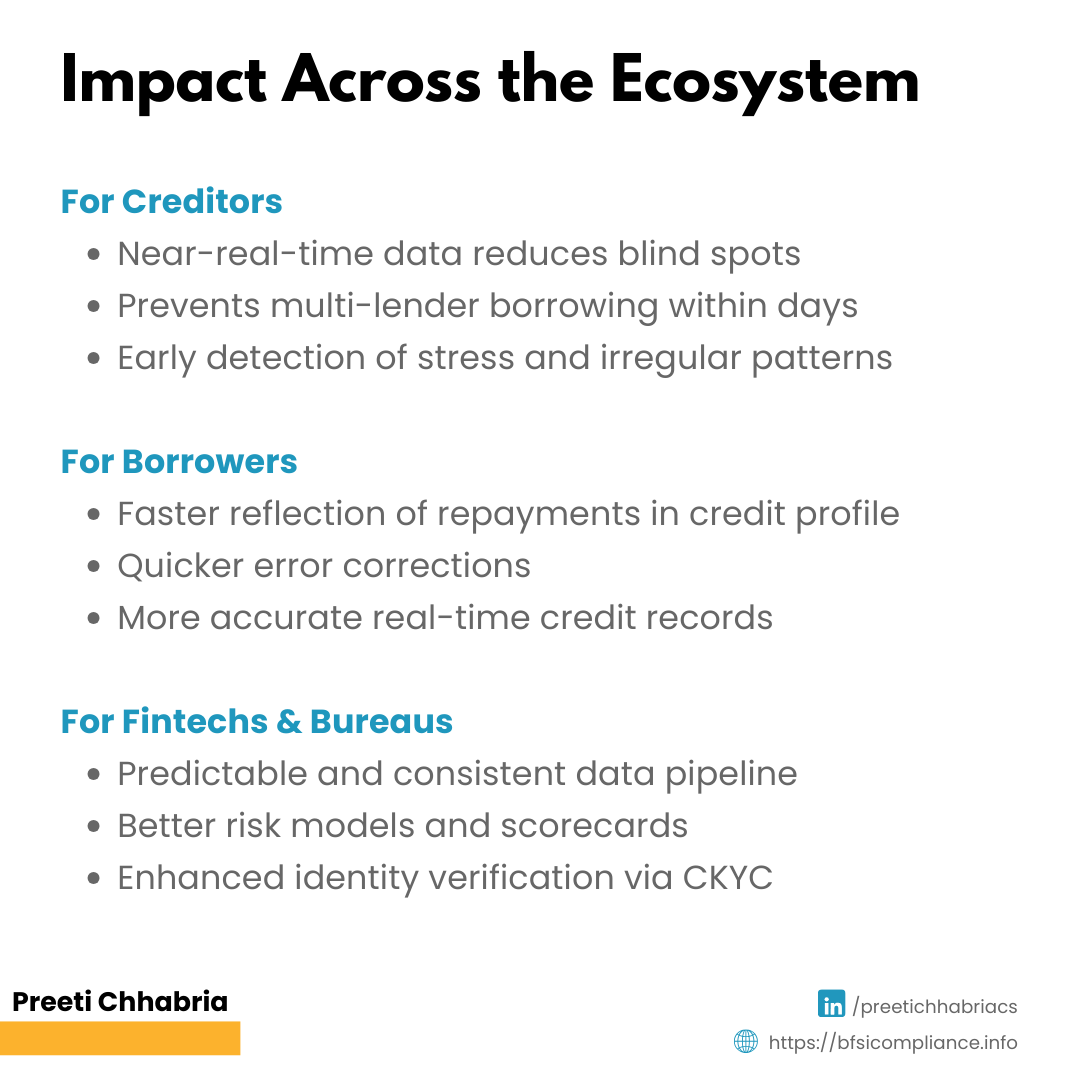

The impact of this shift will be felt across the ecosystem:

- Creditors benefit from fresher and cleaner data, reducing blind spots and fraud risks

- Borrowers benefit from faster reflection of repayments and corrections

- Fintechs and credit bureaus benefit from more stable and predictable data flow

Overall, these amendments move India’s credit infrastructure closer to real-time accuracy, making lending safer, fairer, and more transparent.

DAKSH Portal: It is the centralised supervisory platform through which the Reserve Bank monitors compliance, collects regulatory data, and flags delays or deficiencies across supervised entities. It enables real-time tracking of reporting behaviour, making supervision faster, more consistent, and fully digital.

Follow me on LinkedIn for more information and subscribe for updates on compliance, NBFCs, BFSI, etc.