NBFCs have played a significant role in India’s development. They play a crucial role in the financial system that banks do not necessarily provide. They have grown in size and complexity and, thus, need robust regulatory treatment. To this end, the RBI has brought new regulations for NBFCs.

History of Scale-Based Regulations

On 19th October 2023, RBI published Master Direction – Reserve Bank of India (Non-Banking Financial Company – Scale Based Regulation) Directions 2023 (or SBR Master Directions). These replaced earlier frameworks: (i) Non-Banking Financial Company–Non-Systemically Important Non-Deposit taking (Reserve Bank) Directions, 2016, and (ii) Non-Banking Financial Company–Systemically Important Non-Deposit taking Company and Deposit taking Company (Reserve Bank) Directions, 2016.

On 4th December 2020, RBI, in its Statement on Developmental and Regulatory Policies, announced the need for a revised framework for regulating NBFCs. A month later, on 22nd January 2021, it released a discussion paper titled ‘Revised Regulatory Framework for NBFCs – A Scale-based Approach’. Based on the inputs from stakeholders, on 22nd October 2021, it was announced that the new guidelines would come into effect on 1st October 2022. However, some rules around IPO funding will be applicable from 1st April 2022 onwards.

Old Regulations

Previously, NBFCs were classified based on i) the type of liabilities and asset size; and (b) the nature of activities of NBFCs.

In the former, they were divided into deposit-accepting (also called NBFC-D) and non-deposit-accepting NBFCs (NBFC-ND). Further, based on the asset size, NBFC-NDs were classified as systematically important (NBFC-ND-SI) and non-systemically important NBFCs (NBFC-ND). If the asset size was less than Rs. 500 crore, it was classified as NBFC-ND and if it exceeded Rs. 500 crore, it was called NBFC-ND-SI.

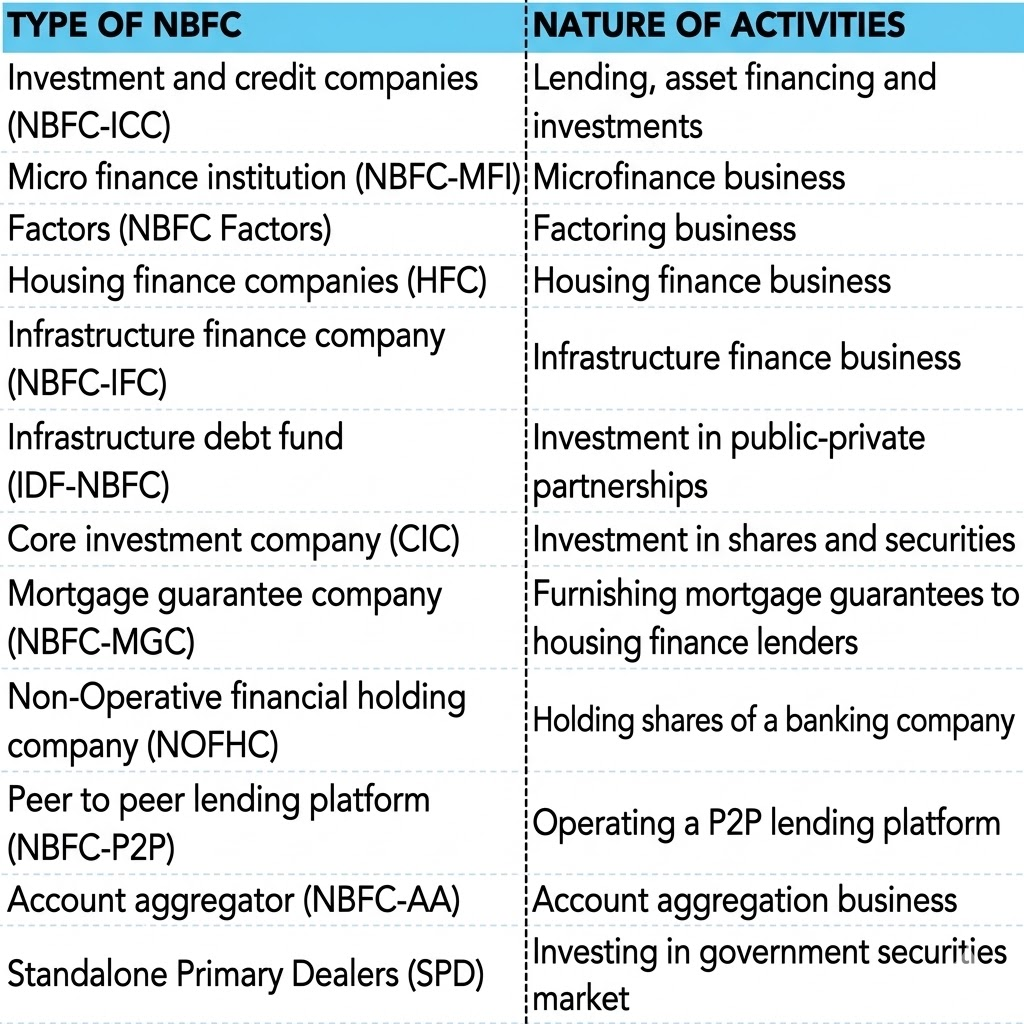

In the latter, they were divided into various types depending on the business. For example, if it engaged in microfinance, it was called a Microfinance Institution (NBFC-MFI), or if the business was investing in shares and securities, they were called Core Investment Companies (CIC), and so forth. The following table lists out different types of NBFCs based on the nature of activity:

New Regulations

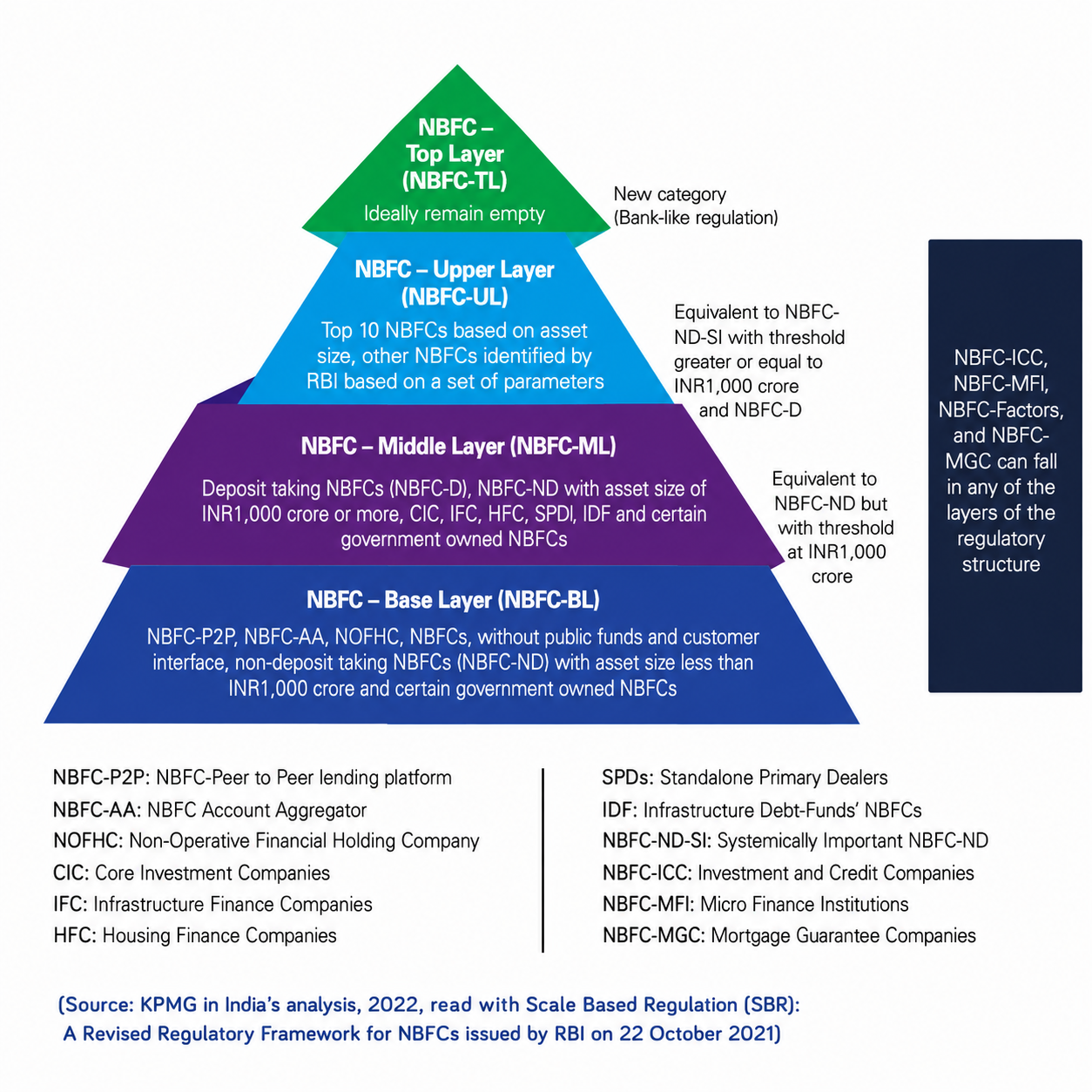

From 1st October 2022, the Reserve Bank of India (RBI) introduced the Scale-Based Regulatory (SBR) Framework for NBFCs. Under this framework, NBFCs are classified into four regulatory layers based on their size, activity, and perceived risk profile — namely the Base Layer, Middle Layer, Upper Layer, and Top Layer.

Here’s a snapshot of the new scale-based regulations:

Base Layer

The Base Layer includes relatively smaller NBFCs with lower risk exposure. It covers:

• Non-deposit accepting NBFCs (including NBFC-ICC, NBFC-MFI, NBFC-Factor, and NBFC-MGC) with asset sizes below INR 1,000 crores

• NBFC-P2P

• NBFC-AA

• NOFHC

• NBFCs not availing public funds and not having any customer interface

Among these, only non-deposit accepting NBFCs may be shifted to other regulatory layers based on their growth and risk profile.

Middle Layer

The Middle Layer consists of NBFCs with relatively higher asset sizes and greater systemic importance. It includes:

• NBFC-D

• Non-deposit accepting NBFCs (including NBFC-ICC, NBFC-MFI, NBFC-Factor, and NBFC-MGC) with asset sizes above INR 1,000 crores

• HFC

• CIC

• NBFC-IFC

• IDF-NBFC

• SPD

Most NBFCs in this layer may be shifted to the Upper Layer, except IDF-NBFCs and SPDs, which will always remain in the Middle Layer.

Upper Layer

The Upper Layer includes NBFCs specifically identified by the RBI for enhanced regulatory supervision. Additionally, the top 10 NBFCs based on asset size will always remain in this category.

Once an NBFC is classified under the Upper Layer, it must remain there for a minimum period of five years, irrespective of whether it continues to meet the scoring criteria.

Top Layer

The Top Layer is expected to remain largely empty and will be populated only if the RBI identifies certain NBFCs as carrying substantial systemic risk.

NBFCs placed in this layer will be subject to:

• Enhanced supervisory scrutiny

• Stricter compliance requirements

• Higher capital requirements

The SBR framework has been introduced to address the evolving risk profile of NBFCs and strengthen the stability of the financial system. In addition, the RBI continues to introduce amendments and regulatory updates from time to time to ensure effective governance and risk management across the sector.

Experts across the financial ecosystem have widely welcomed these regulations as a significant step toward strengthening the NBFC sector.

Follow me for more insights and updates on NBFC regulations and compliance.