India’s digital banking revolution isn’t just a fintech success story — it’s becoming a benchmark for the world.

In recent weeks, four major developments have highlighted both the pace of progress and the proactive nature of the regulator in building trust in the system. Let’s break them down.

1. Indian Banks Outperform Global Peers in Digital Banking

Indian banks have made remarkable progress in digital transformation, as highlighted in Deloitte’s 2024 Digital Banking Maturity (DBM) report.

The study examined 349 banks across 44 countries. The top 10% of global banks earn the title of “Digital Champions,” and 9 out of 12 leading Indian banks achieved this recognition.

India’s DBM score increased by 16 percentage points, rising from 43% in 2022 to 59% in 2024, surpassing the global average. The biggest improvement came from day-to-day banking services, which alone contributed 10 percentage points to the overall growth.

Despite this success, Indian banks still have room for improvement, particularly in ecosystem integration and product cross-selling, where global leaders continue to outperform.

However, India remains well-positioned for further growth due to strong digital public infrastructure, supportive regulations, and evolving consumer preferences.

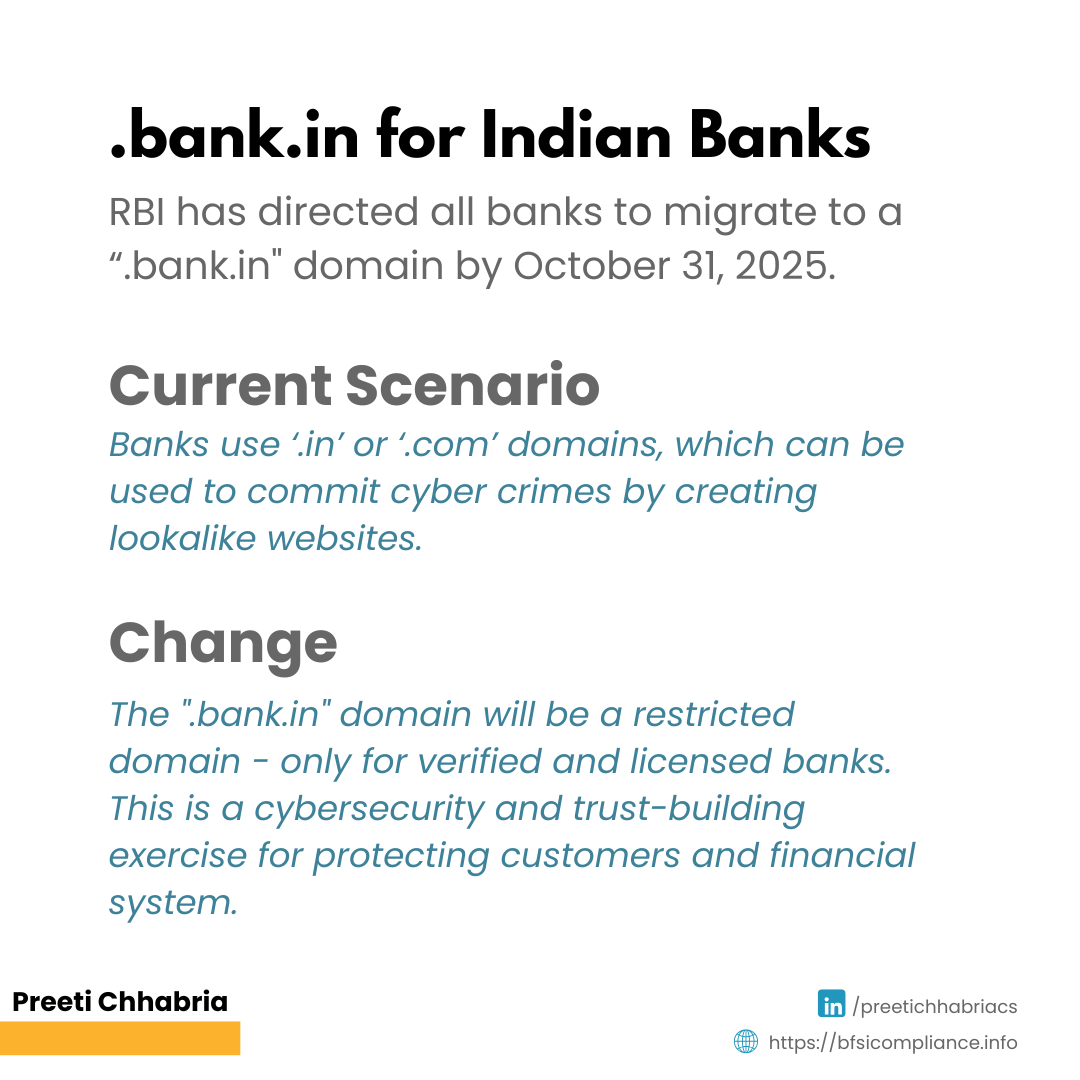

2. RBI Wants Banks to Move to “.bank.in” Domains

In a significant cybersecurity initiative, the RBI has directed all banks to migrate to the “.bank.in” domain by October 31, 2025. This will serve as the official digital identity for banks operating in India.

Banks will also be required to update all public-facing communication and marketing material accordingly.

Why Does RBI Want This Change?

Currently, banks operate on “.in” or “.com” domains, which can easily be imitated by fraudsters through lookalike websites.

The “.bank.in” domain will be a restricted and verified domain issued only to licensed banks under strict regulatory oversight.

This move is aimed at:

● Reducing phishing and cyber fraud

● Strengthening customer trust

● Enhancing digital security in banking

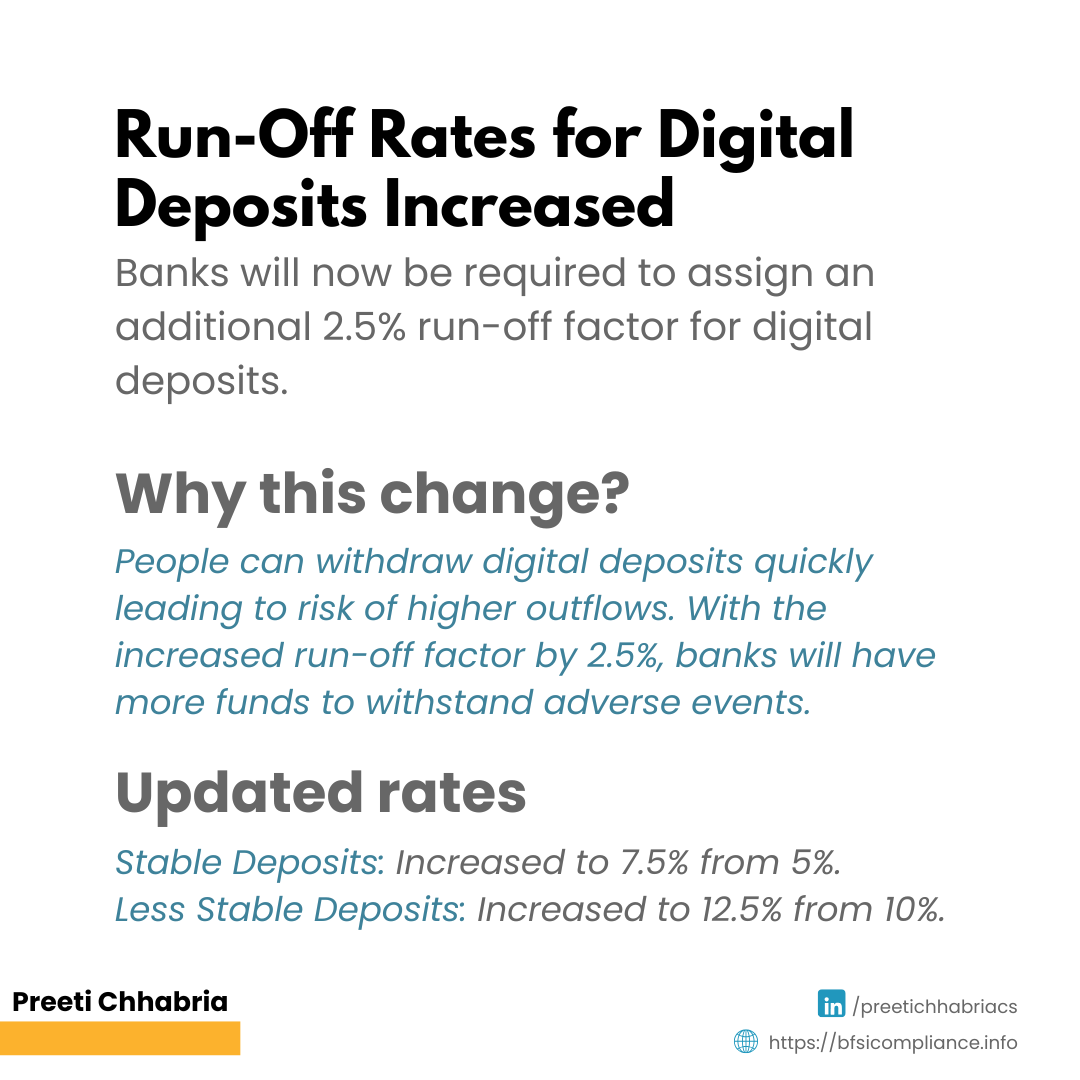

3. RBI Increases Run-Off Rates for Digital Deposits

In response to rapid digitalisation, the RBI has introduced important updates to Liquidity Coverage Ratio (LCR) norms.

Banks will now be required to assign an additional 2.5% run-off factor for digital deposits.

This highlights the RBI’s view that while digital banking improves convenience, it also increases liquidity risks due to faster withdrawal capabilities.

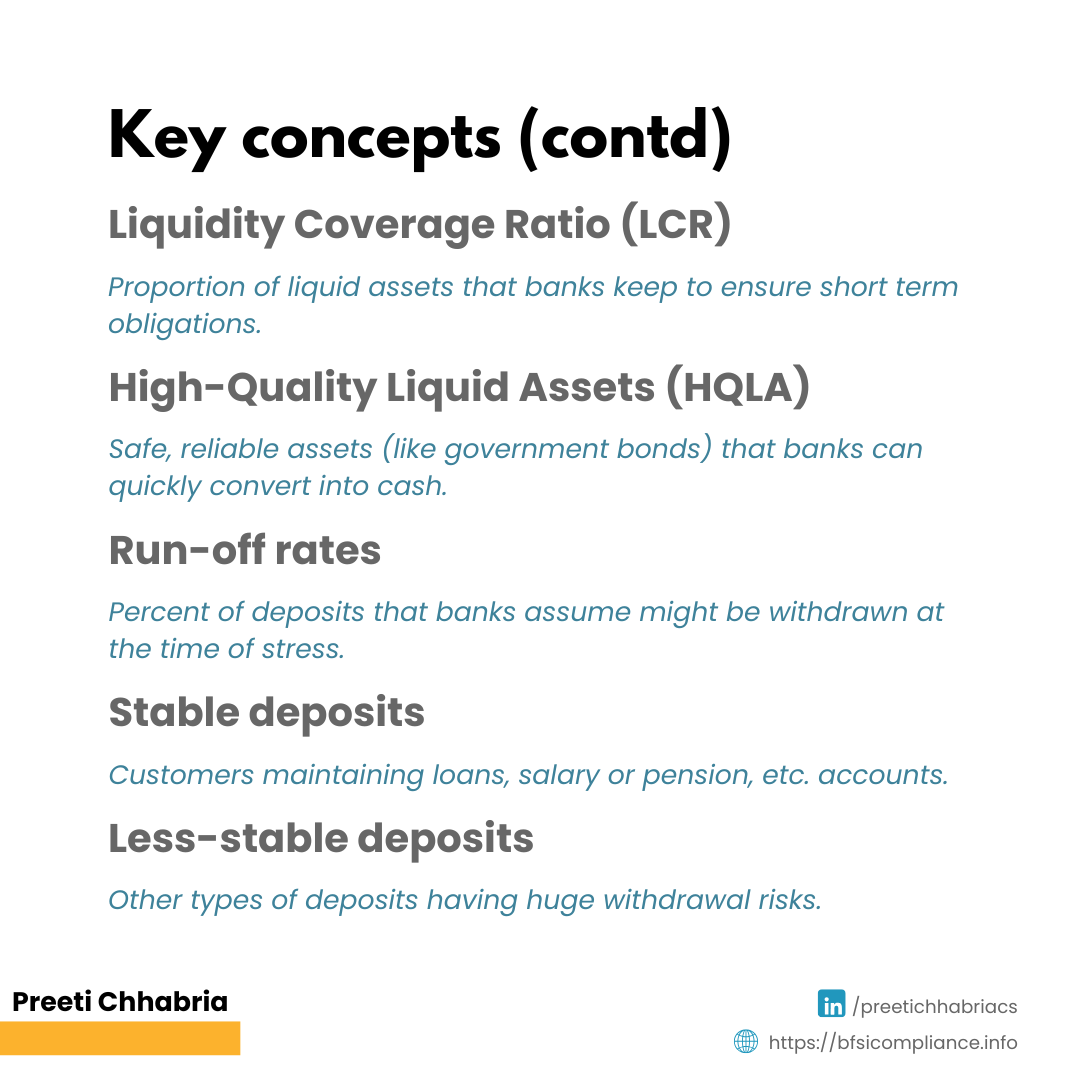

Key Concepts

Liquidity Coverage Ratio (LCR)

A regulatory requirement ensuring that banks maintain sufficient liquid assets to survive 30 days of stressed cash outflows.

High-Quality Liquid Assets (HQLA)

Safe and highly liquid assets, such as government securities, that can quickly be converted into cash with minimal loss.

Run-Off Rates

Run-off rates represent the percentage of deposits that banks assume may be withdrawn during periods of financial stress.

Updated Run-Off Rates for Internet and Mobile Banking Deposits

● Stable Deposits: Increased from 5% to 7.5%

● Less Stable Deposits: Increased from 10% to 12.5%

Stable deposits generally include salary-linked or pension-linked accounts, or customers maintaining broader banking relationships such as loans.

Deposits without such relationships are classified as less stable due to higher withdrawal risk.

Why Has RBI Increased Run-Off Rates?

Internet and mobile banking enable customers to transfer or withdraw funds instantly, increasing the possibility of sudden outflows during uncertain periods.

The revised norms are intended to:

● Improve liquidity preparedness

● Strengthen banking resilience

● Align Indian regulations more closely with global standards

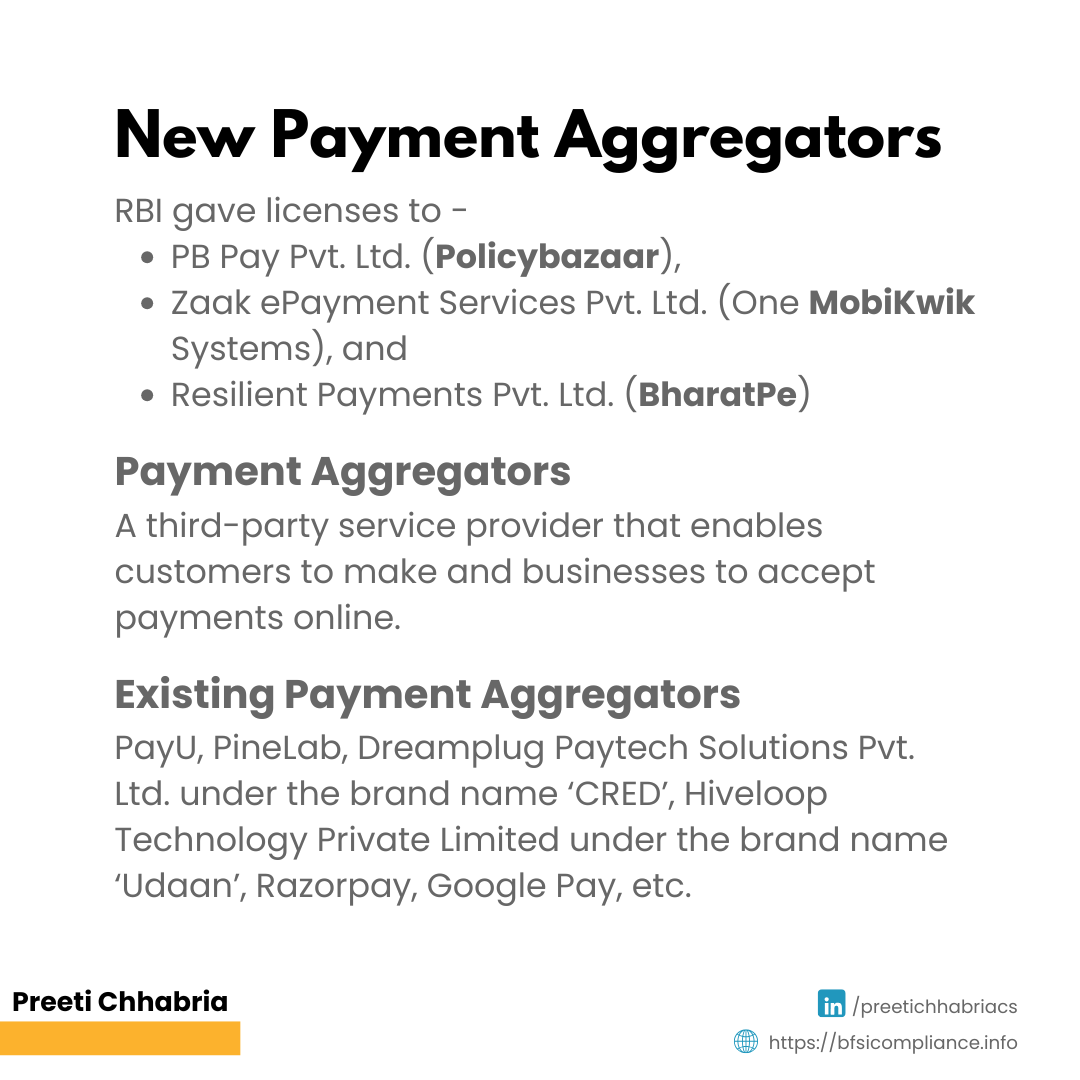

4. PB Pay, ZaakPay and Resilient Payments Receive RBI’s Payment Aggregator License

In another important development, the RBI granted Payment Aggregator (PA) licenses to:

● PB Pay Private Limited — subsidiary of PB Fintech (Policybazaar)

● Zaak ePayment Services Private Limited — subsidiary of One MobiKwik Systems

● Resilient Payments Private Limited — subsidiary of BharatPe

What Is a Payment Aggregator?

A payment aggregator is a third-party service provider that enables businesses to accept online payments through multiple payment methods, including:

● Debit and credit cards

● UPI

● Net banking

● Wallets

● EMIs

● E-mandates

What Does a PA License Allow?

A Payment Aggregator license enables fintech companies to:

● Onboard merchants

● Facilitate digital transactions

● Act as intermediaries between buyers, sellers, and banks

Some of the existing payment aggregators are: PayU, PineLab, Dreamplug Paytech Solutions Private Limited under the brand name ‘CRED’, Hiveloop Technology Private Limited under the brand name ‘Udaan’, Razorpay, Google Pay, etc.

Follow me on https://www.linkedin.com/in/preetichhabriacs/ for more information and subscribe for updates on compliance, NBFCs, BFSI, etc.

Subscribe to my newsletter directly to your email inbox: https://bfsicompliance.info/subscribe-for-alerts/