In the rapidly evolving financial landscape, Know Your Customer (KYC) compliance stands as a critical pillar for financial institutions. It helps financial institutions check the background of the customer. It also helps maintain customers’ risk profiling. Integrating KYC within a robust Governance, Risk Management, and Compliance (GRC) framework streamlines compliance processes and fortifies institutions against financial crimes and operational risks.

The Importance of KYC

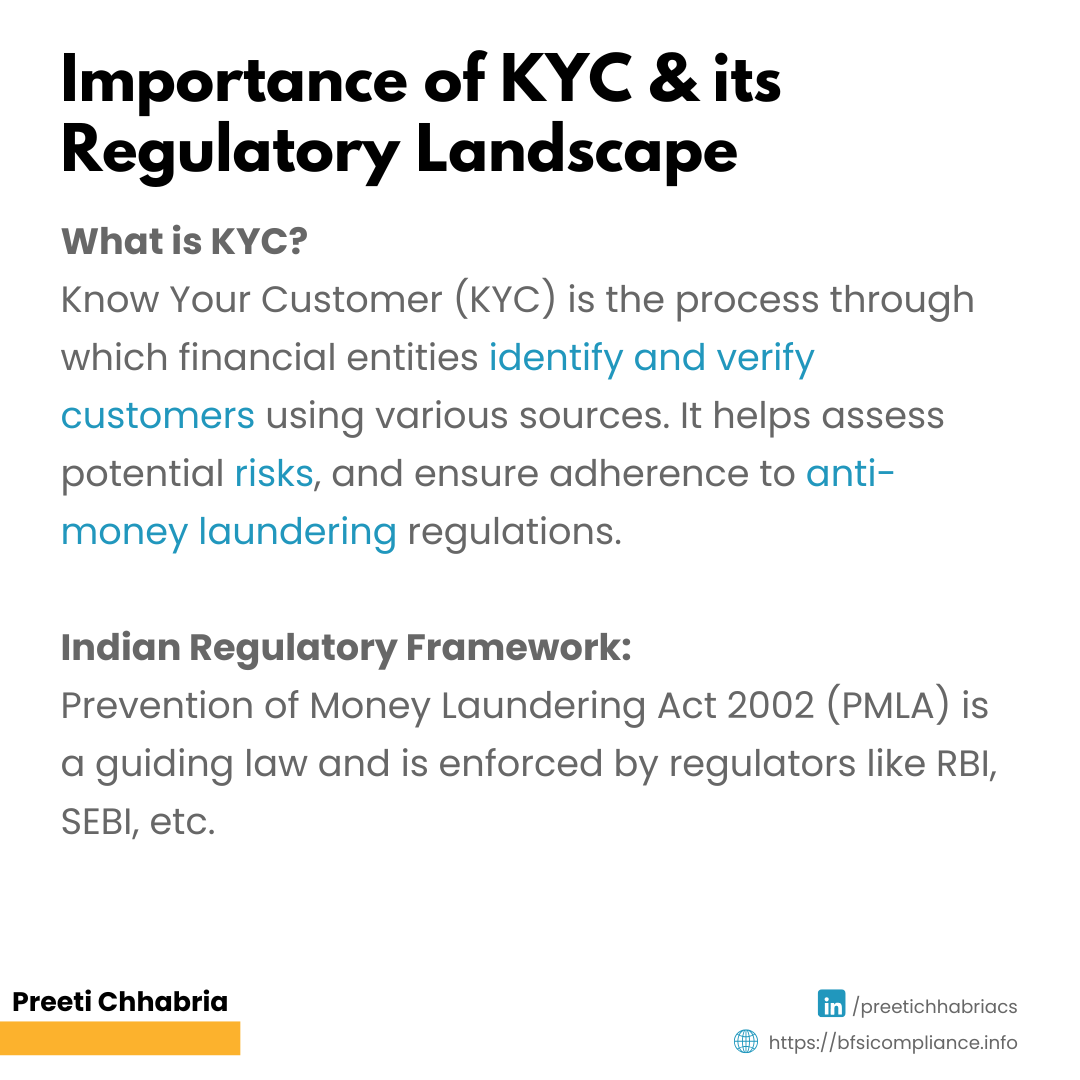

KYC encompasses the processes by which financial institutions verify the identity of their clients, assess potential risks, and ensure adherence to anti-money laundering regulations. Effective KYC practices are essential for deterring activities such as financial crimes, money laundering and terrorist financing; legal compliance; and building trust among customers and stakeholders.

Regulatory Landscape for KYC Compliance in India

India’s KYC regulations aim to curb financial crimes like money laundering and fraud. Anchored in the Prevention of Money Laundering Act of 2002 (PMLA) and enforced by RBI, SEBI, and IRDAI, the KYC framework ensures identity and address verification before accessing financial services.

KYC Process

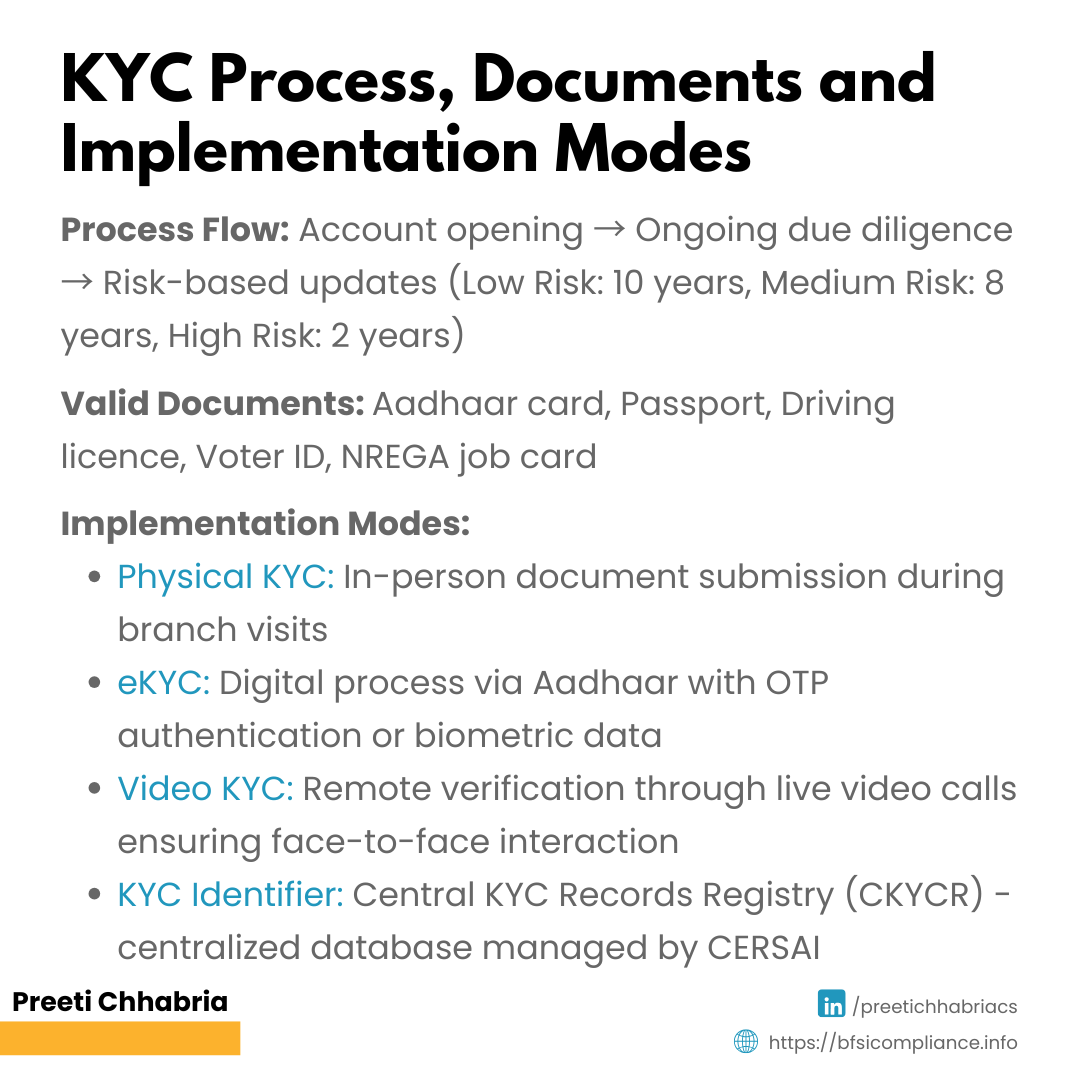

The KYC process begins while opening any type of account with any financial institution – say opening a savings account, a salary or pension account or even a loan account. Then, every few years, the financial institution asks the customers to update these records.

Customer risk profiles determine KYC update frequency: every 10 years (low risk), 8 years (medium), and 2 years (high). Institutions must ensure compliance or face regulatory penalties. However, recently, RBI Governor Sanjay Malhotra urged banks to stop repeatedly asking customers for KYC documents, emphasising the use of a central database to ease the process and reduce inconvenience.

Here is the List of Valid KYC Documents

1. Proof of Identity (Any One of the Following Documents)

• Aadhaar card

• Passport

• Driving licence

• Voter ID

• PAN card

• Photo ID cards issued by the Central or State government entities, public financial institutions and public sector undertakings

2. Proof of Address (Any One of the Following Documents)

• Voter ID card

• Driving licence

• Passport

• Utility bills, such as water bill, electricity, gas bill, or telephone bill (not older than one month)

• Ration card

• Rental agreement

• Sale deed

• Passbook or bank statement containing the address

Modes of KYC

While procuring KYC is mandatory, the financial institutions can obtain those records through various modes such as:

• Physical KYC: This traditional method involves in-person submission of identity and address proof documents, usually during branch visits.

• eKYC: Enabled by Aadhaar, this digital process verifies identity via OTP authentication or biometric data, allowing faster and paperless onboarding.

• Video KYC: A remote verification process where customers complete KYC through a live video call, ensuring face-to-face interaction without physical presence.

• CKYC (Central KYC): A centralised database managed by CERSAI that stores verified KYC records, enabling institutions to access existing customer data without repeating the process.

GRC in KYC

Integrating KYC processes into GRC frameworks is essential for organisations aiming to enhance operational efficiency, ensure regulatory adherence, and mitigate risks. This integration fosters a unified approach to managing compliance risks, promoting transparency and accountability across all levels of the organisation.

Here are some advantages of integrating GRC framework into the KYC process:

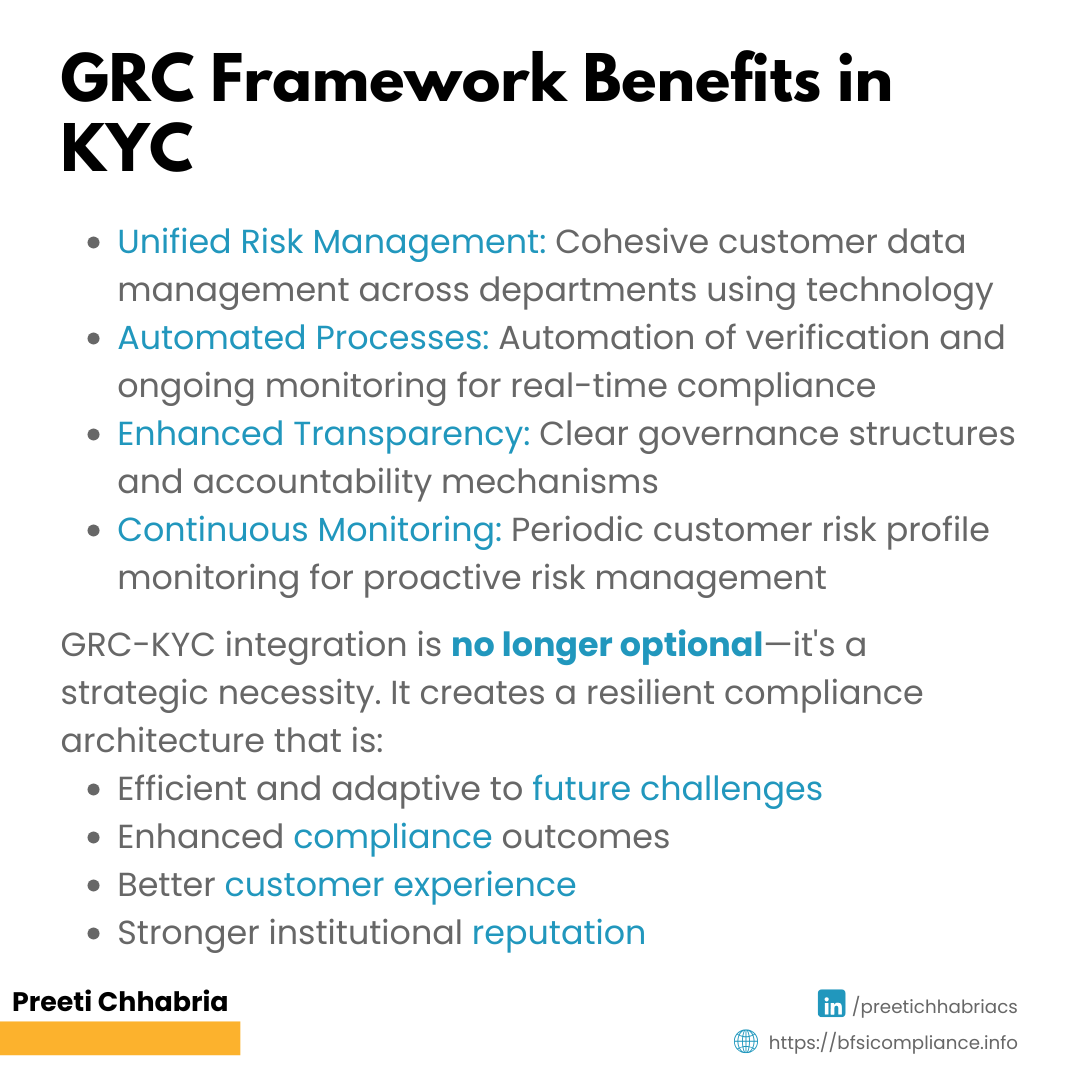

1. Unified Risk Management

A lot of times, customer data is saved across departments, hampering a unified view of customer information and leading to inefficiencies. Using technology and a robust GRC framework, organisations can manage risks across various departments cohesively. This alignment ensures that KYC procedures are consistent with the organisation’s overall risk management strategies, facilitating the identification and mitigation of potential compliance risks more effectively.

2. Automated Processes

Leveraging technology within GRC frameworks allows for the automation of numerous KYC tasks, such as customer verification and ongoing monitoring. Automation minimises manual errors, enhances efficiency, and ensures real-time compliance with evolving regulations.

3. Enhanced Transparency and Accountability

A well-integrated GRC framework establishes clear governance structures and accountability mechanisms. This clarity ensures that all stakeholders comprehend their roles in maintaining KYC compliance and are held accountable for any lapses.

4. Continuous Monitoring

The GRC framework enables discipline across the organisation, which can help it monitor customer risk profiles periodically. This capability enables organisations to respond promptly to changes in customer behaviour or regulatory requirements, maintaining a proactive stance against potential risks.

5. Regulatory Compliance

Integrating KYC into a GRC framework ensures consistent adherence to regulatory standards and mitigates financial and reputational losses due to non-compliance.

Conclusion

In today’s environment of complex financial operations and dynamic regulatory requirements, integrating KYC into a GRC framework is no longer optional—it is a strategic necessity. While KYC ensures that financial institutions know their customers and assess risk, GRC provides the structure, tools, and accountability to manage that knowledge effectively. When combined, they create a resilient compliance architecture that is not only efficient but also adaptive to future challenges.

For Indian financial institutions, where regulatory scrutiny is rising and digital onboarding is expanding, embracing GRC-KYC integration can significantly enhance compliance outcomes, customer experience, and institutional reputation.