Why G, R, and C Should Be Your Company’s Best Friends

All the legal experts reading this know these words by heart. But for the uninitiated, let me simplify these concepts.

Assume G, R, and C are my closest friends.

● G is the wisest. It takes all the big decisions and ensures fairness and accountability.

● R is daring — always planning for the worst but knows how to walk the tightrope.

● C is the cautious one — slightly boring, but never lands us in trouble.

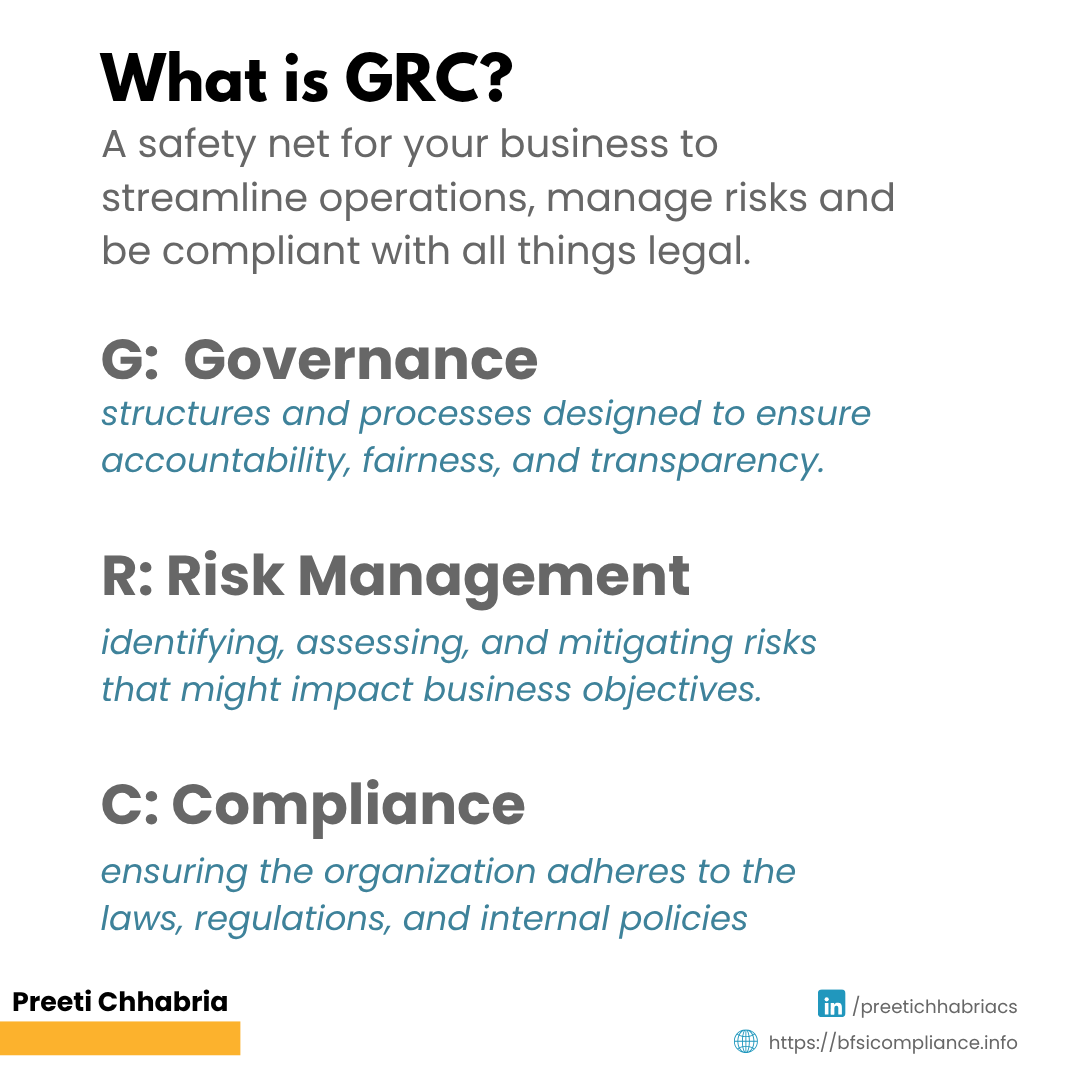

Now, in the corporate world, they are nothing but Governance, Risk Management, and Compliance. Let us learn them one by one.

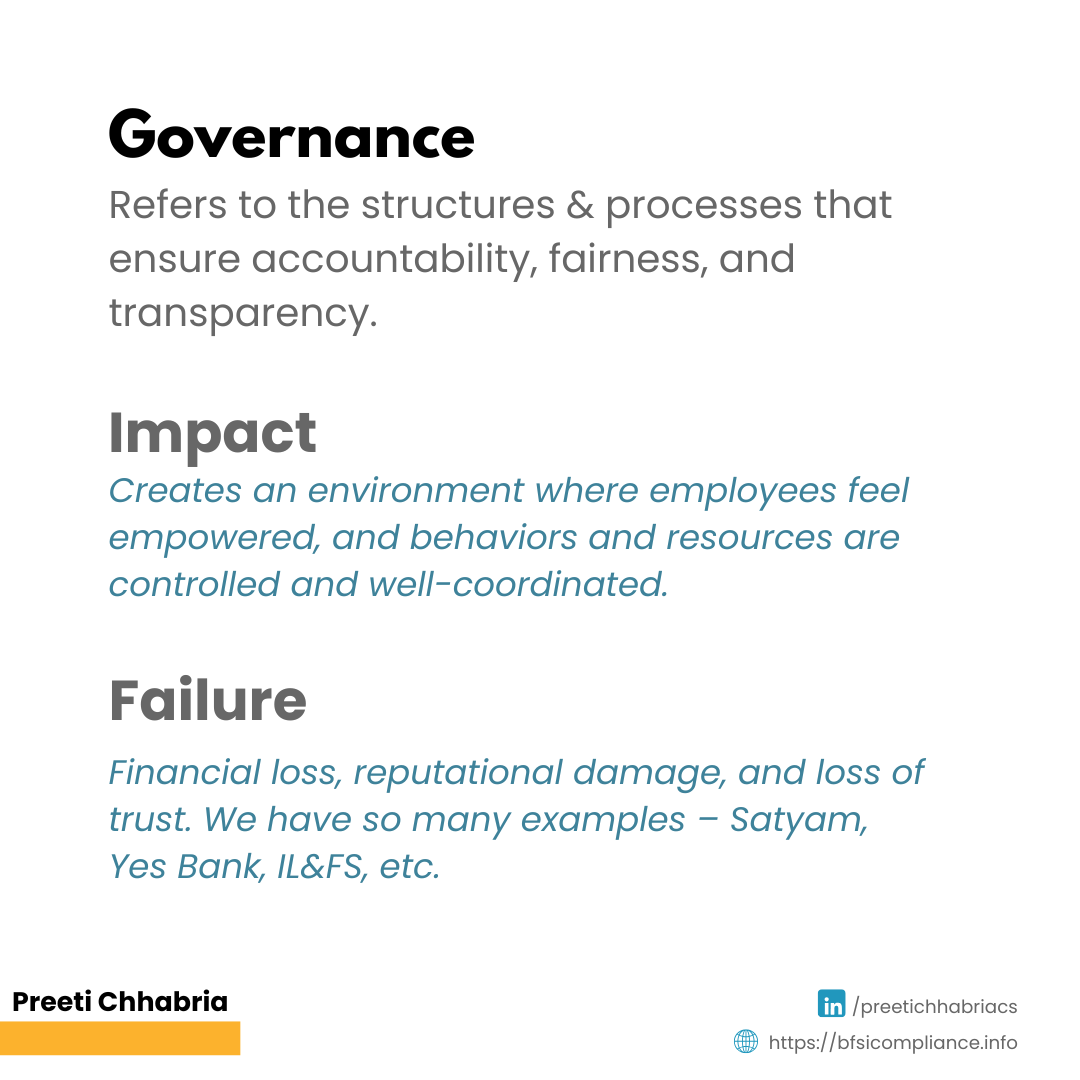

Governance: The Pillar of Accountability

Governance refers to the systems and processes that ensure transparency, fairness, and accountability in a business. It ensures that decision-making is ethical and aligned with the company’s long-term goals.

Lapses in governance often lead to catastrophic outcomes. India has seen many instances of governance failures like Satyam, Yes Bank, IL&FS, etc. When governance fails, trust disappears and rebuilding that trust takes years, if not decades.

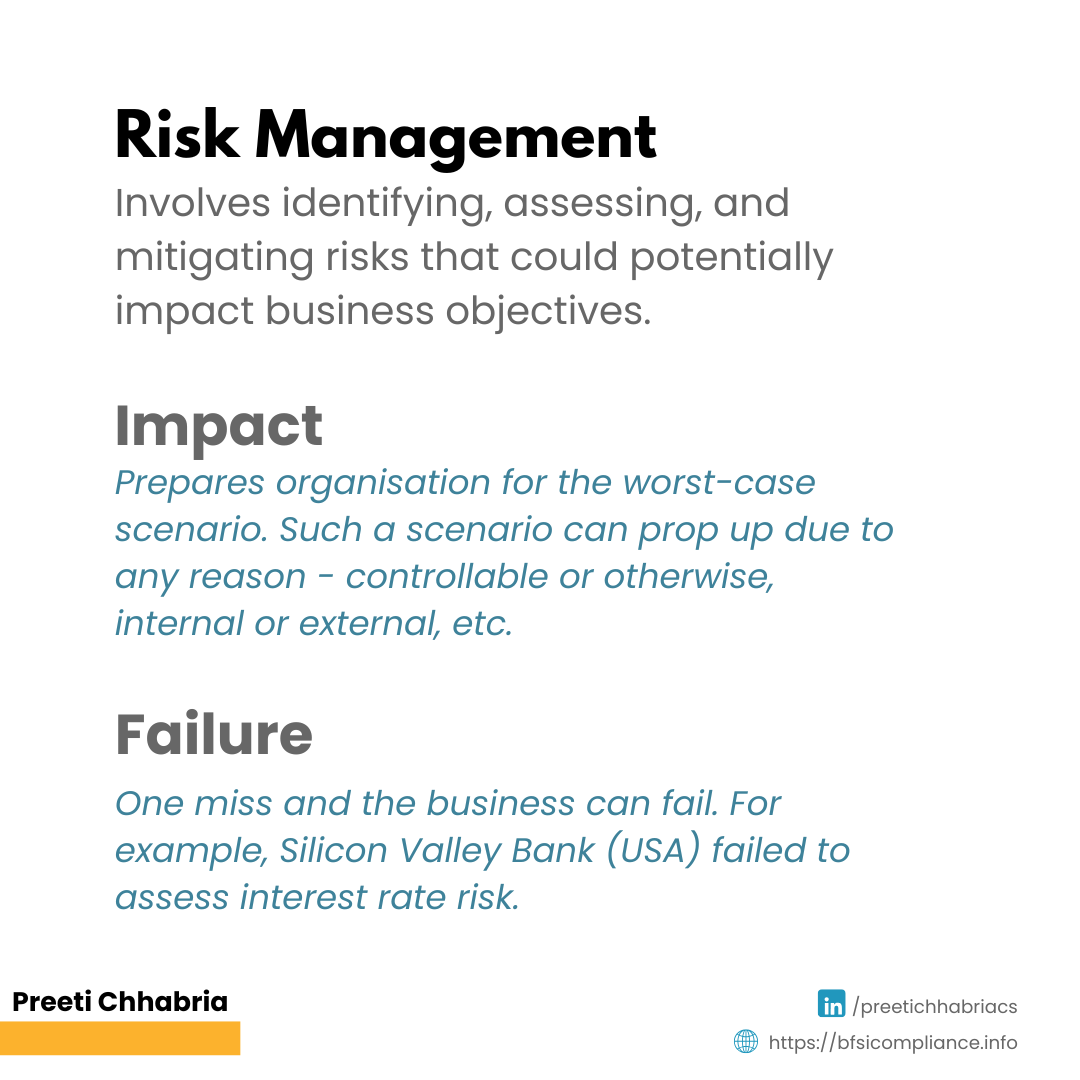

Risk Management: Preparing for the Worst

Risk management is about identifying, assessing, and mitigating risks — whether they are operational, market-related, credit-related, or reputational.

Take Silicon Valley Bank — a textbook example of how interest rate risk was grossly underestimated. Despite having a good credit rating, the bank collapsed due to poor risk forecasting.

One area that deserves special attention under risk management is credit risk. It’s the risk that borrowers may fail to repay loans, which can even turn into bankruptcy.

Types of Credit Risks

● Default Risk – When a borrower fails to make payments, turning into a Non-Performing Asset (NPA).

● Concentration Risk – When too much exposure is focused on one sector or borrower group.

● Country Risk – Losses due to political or economic instability in the borrower’s country.

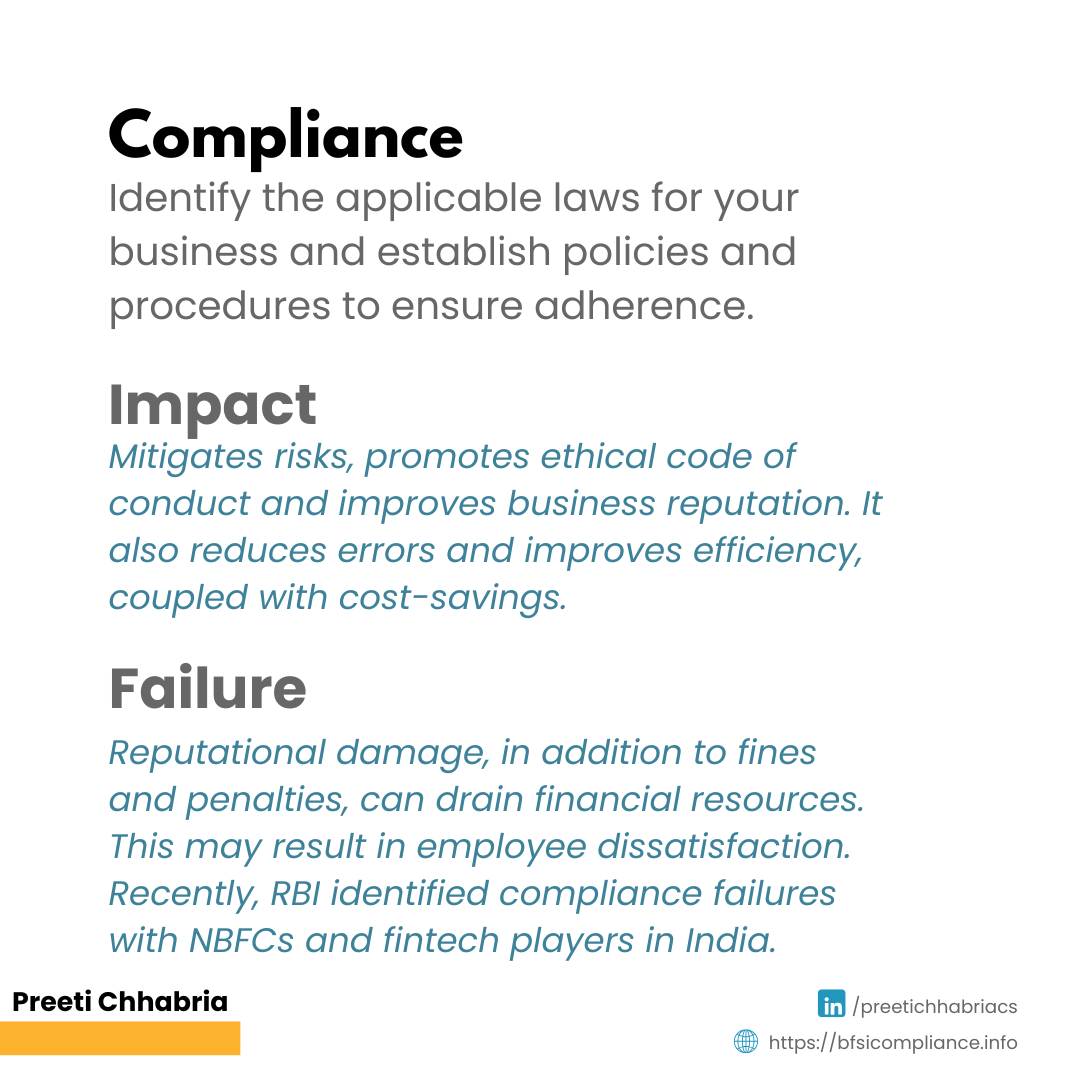

Compliance: Adhering to Rules Before It’s Too Late

Compliance ensures that organisations follow rules, laws, and ethical standards, internal as well as external. Recently, RBI flagged several NBFCs and fintechs for non-compliance with KYC norms, money laundering safeguards, and data privacy laws.

Compliance also ensures smooth coordination with regulators and helps companies avoid penalties, investigations, or even shutdowns. Non-compliance carries huge reputational and financial risks.

How G, R, and C Come Together

A well-designed GRC framework ensures that:

● Governance structures are robust

● Risks (like credit, market, cyber, etc.) are proactively managed

● Compliance is maintained across all operations

It also automates reporting, brings transparency, and allocates responsibilities across teams. This becomes especially important when dealing with complex risks like credit defaults or data breaches.

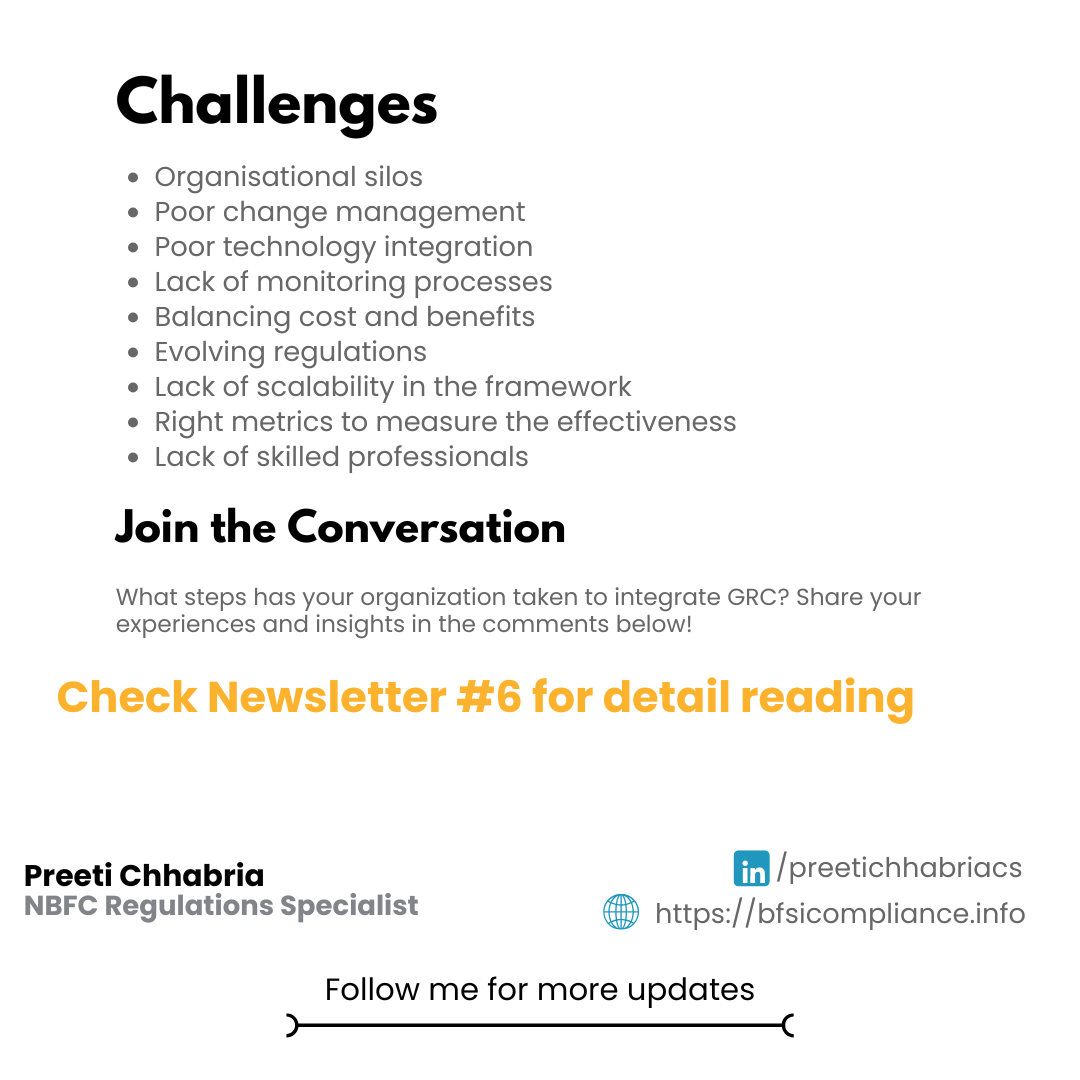

But building this framework isn’t easy. There are challenges such as inefficient data management, lack of sophisticated risk tools, and cumbersome internal reporting structures.

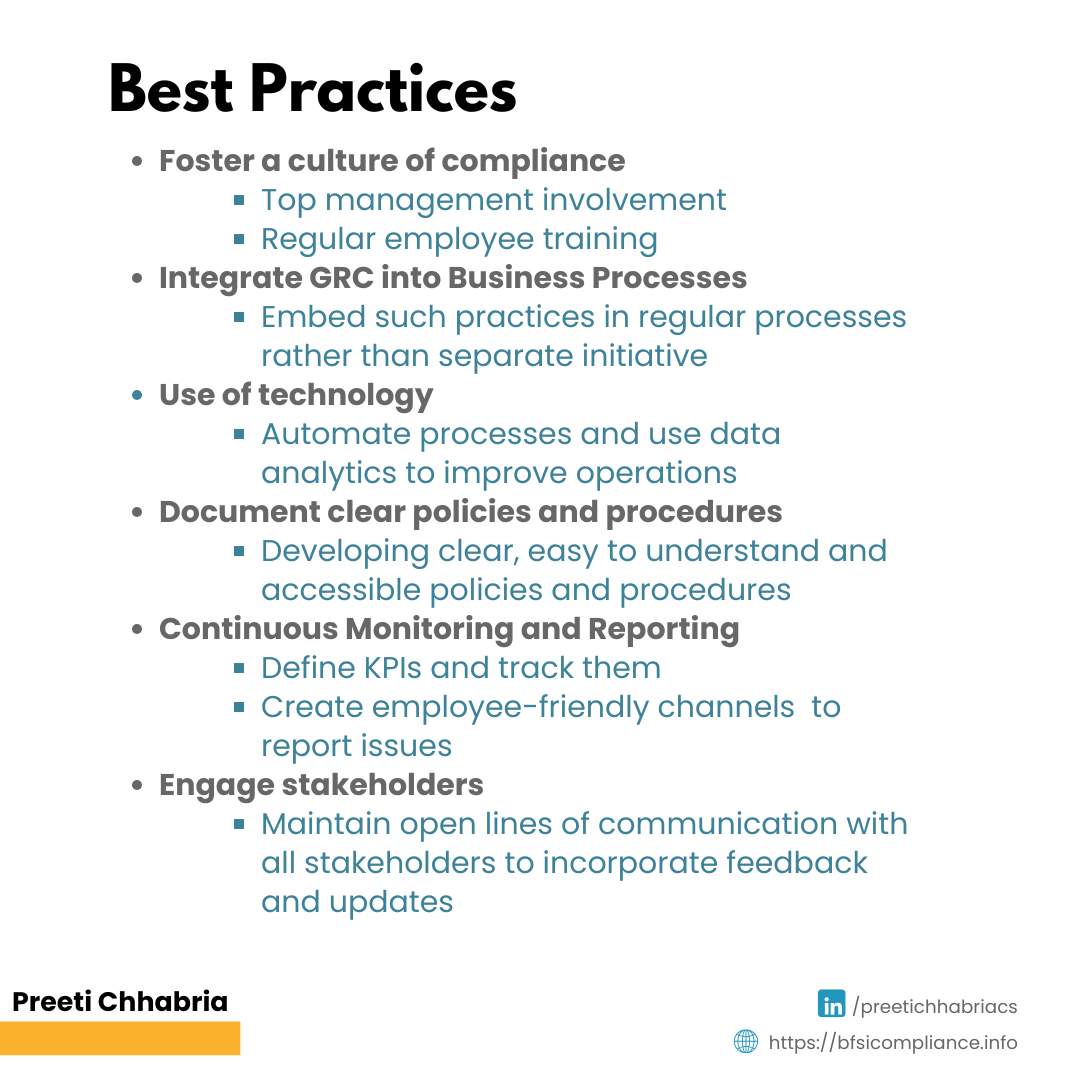

Best Practices

To truly embed GRC into the culture and overcome challenges, organisations must:

● Invest in strong data and risk analytics systems

● Simplify internal processes and reporting

● Train employees on compliance and governance

● Build early-warning systems for credit and operational risks

● Keep updating risk mitigation strategies

Final Thoughts

The collapses of IL&FS, Lehman Brothers, and Silicon Valley Bank showed us how fragile the system can be without proper governance, risk foresight, and regulatory compliance.

In today’s volatile world, G, R, and C aren’t just frameworks — they’re your best friends in business. Befriend them, and they’ll help you stay out of trouble, navigate crises, and build long-term credibility.

Follow me on https://www.linkedin.com/in/preetichhabriacs/ for more information and subscribe for updates on compliance, NBFCs, BFSI, etc.

Subscribe to my newsletter directly to your email inbox: https://bfsicompliance.info/subscribe-for-alerts/